Dave Erfle – PM Stocks Starting To Diverge From The Markets and Comments On The Gold Standard Ventures “Take-Under”

Dave Erfle, Founder and Editor of The Junior Miner Junky joins us to shares opinion on if the gold stocks are truly diverging from the US markets. Taking it a step further will these stocks be able to breakout to the upside when everything else continues to breakdown? We also discuss the Orla Mining acquisition of Gold Standard Ventures. Dave calls it a “take-under” referring to the cheap price Orla acquired the asset.

The Dow hit an incredible valuation of almost 45 ounces of gold in 1999/2000 as US GDP hit $10 trillion for the first time. For comparison, the Dow topped at less than 20 ounces of gold in 1929 and reached something like 28 in the late 1960s.

The only Dow:Gold peak that’s been at all comparable to the 2000 peak happened in mid 2018 when the Dow reached 22 ounces of gold and obtained a quarterly overbought RSI reading. That high was just half of the 2000 reading yet was still historically well above the mean.

GDP has more than doubled since 2000 but gold has gone up as much as 8+ fold while M2 money supply has gone up 4.65 fold. In other words, the real economy, net of inflation, has been shrinking for about 22 years. GDP would be over $46 trillion right now (instead of $24 trillion) had the economy kept up with all the M2 money supply growth (counterfeiting/theft).

The quarterly Dow:Gold chart looks ugly and I doubt that will change much by the end of this quarter in less than 2 weeks.

And we have all those prisons and jail cells paid for in advance. Just not good use of tax payer money.

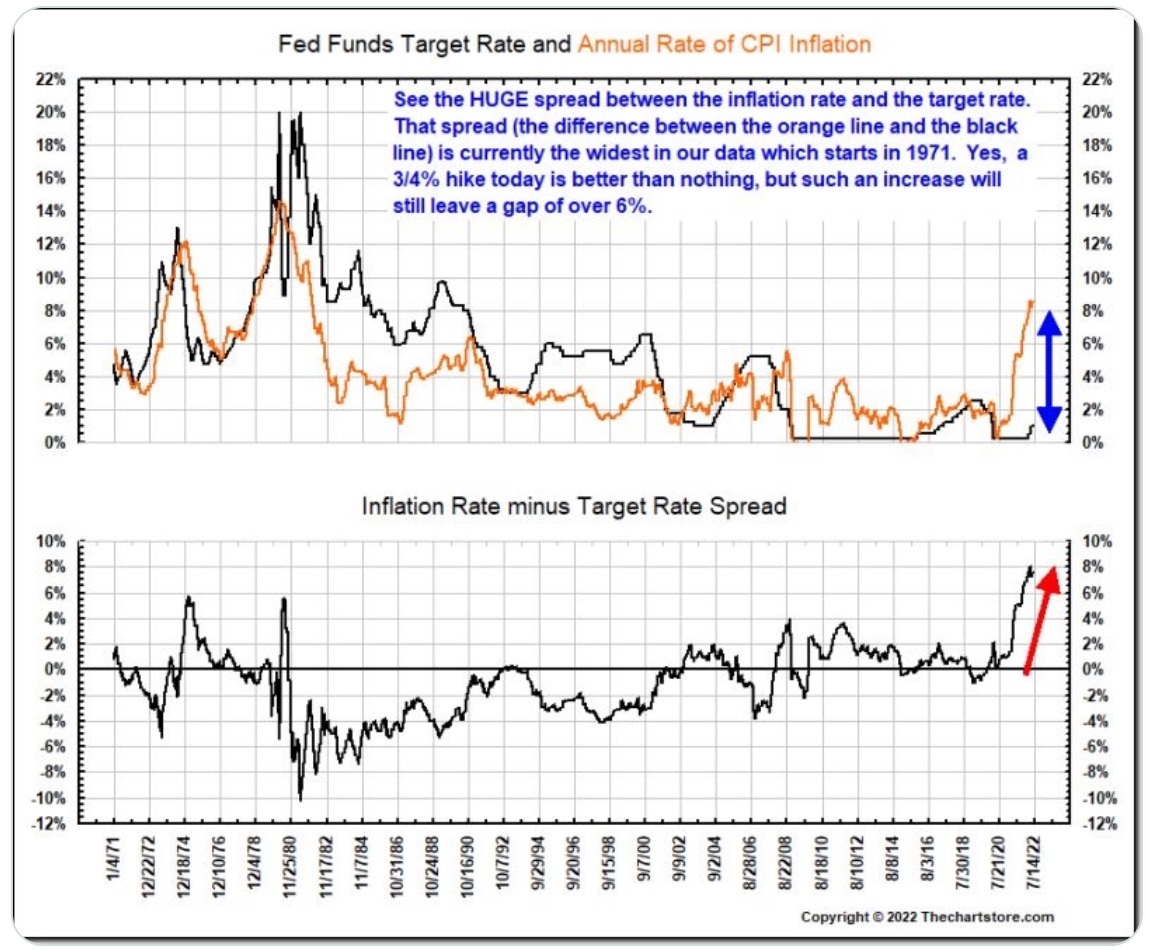

Peter Brandt gets it so the silly “Fed will pivot!” crowd should pay attention: “The Fed has never in modern Fed history been so far behind the curve. Embarrassing. Not only did the Fed create this mess, they are way behind the curve in fixing it. Solution: Fed rate hike by 400 BPs, let stock market collapse and then hit the reset button.”

https://kingworldnews.com/wp-content/uploads/2022/06/KWN-Pet-I-6172022.jpg

{kind=link}

Investors are the last consideration for The Fed as they have reached this point intentionally. They can not be measured by the damage to World economies, but rather the amount of untraceable transfer of wealth to Banking and Corporate interests.

The reset which is not too far off will probably contain debt forgiveness for those that have been enabled to commit the most thefts. Those that played by the rules will go unrewarded.

Raoul Pal thinks the market is wrong and the Fed will pivot fast. He also thinks the Fed can fix the stock market as usual by expanding its balance sheet. He’s in for a surprise he won’t forget.

https://www.youtube.com/watch?v=jOY-4bH38rk&ab_channel=MillionairesInvestmentSecrets

Well, Raoul is not alone in that Dave Erfle, Jordan Roy-Byrne, Brien Lundin, Goldfinger, John Rubino, Craig Hemke, and many others we’ve had on the show believe the Fed will pivot faster than many generalists are expecting, with many projecting it may happen after the September Fed meeting but potentially before the November mid-term elections. Some are looking for a pause in the hiking as the signal, whereas others are expecting a pivot back to cutting towards the end of the year.

The Fed has messaged they’d like to get their Fed funds rate up to about 3.5% – 4%, but with the latest CPI rate clocking in at 8.6% from last month, that would still be a steeply negative real rate of about -4%, and a far cry from getting the Fed funds rate up higher than the rate of inflation.

If they were to be following the Taylor rule the Fed would already have a Fed funds rate of 9%, which is never going to happen because anything above a 4% rate would make their massive debt service on the $9 Trillion on their balance sheet completely unpayable. So yes, they are waaaaay behind the curve and in a desperate game of playing catch up with 75 basis point hikes.

The hilarious part of all this is just last year they said they weren’t even thinking about thinking about hiking rates until 2023, and that inflation would be “transitory.” They blamed everyone but themselves for where the inflation was really coming from, and shrugged it off. The central banksters have been wrongo in the congo about how things would unfold and have a lot of work to do to catch up to the inflation, unless the year-over-year metrics start trending lower in a meaningful way.

We’ll see how it goes…

I don’t think these guys realize how much the market forces the Fed’s actions. This is not 2008 or even 2019/20.

Btw, I don’t think the Fed will get the Fed funds rate above CPI, they’ll pause when the two roughly match. I still think it could happen in the 5 to 6 percent range. They might be staying “behind the curve” because they expect the CPI to drop from the current 9% area by early next year. I can see how it would be preferable (to them) not to raise as aggressively as they did in the ’70s.

The P&F price objective for the 10 year yield is 8.25% but of course there’s no telling how long it will take to get there based on the P&F chart.

Food for thought:

A recession began in January 1980 with inflation at 14.2% and the Fed funds rate was hiked to 15% the following month (from 14%). Then it was hiked again the month after that straight to 20% (March 1980). That May, they lowered the FFR to 11.5% and then to 8.5% that June and the recession ended in July. The following month kicked off another 5 hikes that year (10%, 11%, 12%, 18%, 20%).

This isn’t the 1970s and especially not the late 1970s but we ARE in a new and very young secular bull market in interest rates (secular bear market in bond prices). So be careful with those who look to the last 10 to 20 years for clues about our future.

Good thoughts to mull over Matthew. Yes, I’ve asked people all year long if they felt the Fed was stalling because they expected the year-over-year “base effects” on the government CPI readings to start trending lower. If we think about how high inflation already was by late last spring and summer, it would make sense that they’d start trending down. We did see that slight adjustment down from March at 8.3% to April at 8.1%, but then saw May’s number head back up to 8.6%.

If the point and figure chart on the 10 year yield projects up to 8.25%, then I guess it’s possible that would have the Fed Funds rate up to about 6%-7% roughly. If CPI was to fall from 8.6% down to 6% or lower, then it could be that they do both meet in parity.

This is going to be very interesting to see how it all unfolds, and is sure to make for volatile markets.

I have to wonder if the Fed will be able to pause briefly well before the 10 year hits that 8.25% P&F PO. I wouldn’t bet on it but it’s possible.

It seems the pivoters assume that reverting to cutting would some how be easier for the Fed when in fact the Fed has big problems either way. To cut prematurely now is to fight the new trend whereas all the cuts of recent years/decades have been aligned WITH the dominant trend. The retail investor mantra is “don’t fight the Fed” but the Fed knows that it can’t fight the market, at least not long term.

Agreed Matthew. We’ve asked people about this topic all year long, and some are in the boat that the Fed will cave in an listen to the market, and then others felt the Fed was more concerned about the economic health and job employment and would be fine with more market weakness and will not focus as much on the markets. There is likely a tipping point though, where there would be enough snarling and gnashing of teeth from the general markets and main stream media that the Fed would eventually cave in.

Personally, I’d be more surprised to see the “Powell pivot” right away, and have seen plenty of evidence that the central bank has been far more methodical and slow to respond, so I see a “Powell pause” as far more likely. They’ll likely squeeze off 2 more rate hikes in July and September, and then pause to see how things go (hoping CPI starts trending lower on year-over-year base effects, but will likely take credit for this that their policies are working).

After the next two hikes, it is easy to imagine them messaging that they are going pause and be “data dependent.” This a nebulous position that they’ve used before, and gives them lots of wiggle room and is up for debate which data they’ll care about. There have already been several Fed mouthpieces that have come out and suggested they may pause after the next 2 hikes, so that seems like a more likely scenario, rather than an abrupt turn to cutting rates again.

By next year in 2023, if we are in a more serious or prolonged recession, then I could see them cutting rates again. The reason they want to get the Fed funds up to 3.5%-4% (their target just spoken about this week at the Fed meeting) is that this would be a high enough level from which to start cutting again.

Regardless, by their own admission, most of their policies take 6-9 months before the results start showing up, so even the hikes they’ve done and plan to do, won’t have any substantial effect until much later in the year or next year. Any tempering of the CPI number lower in the interim would have happened regardless without them doing much of anything.

Here’s another to add to the list of the Powell pivoters. Keith Neumeyer of First Majestic Silver.

_________________________________________________________________________________________________________

Keith Neumeyer – Shocked if Gold Not Above $2,000, Fed Has No Control Over Inflation

Stansberry Research – Jun 15, 2022

“If we don’t end this year with gold at $2,100, I’d be pretty surprised,” predicts Keith Neumeyer, First Majestic Silver Corp President and CEO. “Silver will always get buoyed to some degree with gold, and I’m not expecting silver to really rock and roll for a while,” he tells our Daniela Cambone at the Silver & Gold Reception during this year’s 2022 PDAC Conference.

“Unless the Fed goes Volkerish, it will not be able to control inflation,” Neumeyer asserts. “Within six months or so, [the Fed] will start cutting again,” he concludes.

Here’s another Powell pivoter from a few weeks ago.

_______________________________________________________________________________________________

Without A Fed Pivot, The Nasdaq Could Fall

TD Ameritrade Network

“Also, watching TLT to see if the bond market starts to price in a Fed pivot.”

We should keep in mind that it is every bit a potential contrarian signal when the experts all agree. The average retail guy thinks it’s reason for more confidence but that’s a big mistake. I counted 4 dozen well known experts that were bearish stocks in August 2009 and they ended up with no opportunity to cover their shorts without taking a loss. Following the 2011 top in gold, few in the gold space no matter their age or experience were right about anything. Most even thought the stock market was in a bubble around Dow 13,000. Those guys’ mistakes along with my own helped me learn a lot of lessons.

That’s a great point Matthew, and one I completely agree with. When everyone is on the same side of the boat, it generally turns the other direction.

This is something Cory & I have discussed with each other, that with so many pundits convinced that the Fed wouldn’t get far in their rate hikes (most people we talked with projected up to 2% or 3% max) and that they’d reverse course right away, that it seems reasonable to consider the other possibility…. ie. that the Fed would hike up past 3% to more like 3.5-4% (as they are now messaging) and that they may not be as swift to reverse course and start cutting as so many are counting on.

That’s why I personally think it’s more likely they’ll get to the point where they just “pause” and gather more data, without doing either more hikes or start cutting after the September hike is in the books. They could camp out in paused land for a few months, during the mid-term elections in the US, and it would appear they are not taking any partisan sides that way.

I’m not sure if you heard Jordan’s interview from this week, where he unpacked the historical data about the last 13 rate hikes he analyzed, and that in 6 of them, during inflationary periods most of them reversed course from hiking to cutting in a 1-2 month period. I felt he outlined the best argument for the swift reversal and Powell pivot thesis so far.

Who knows what will actually happen, but Jordan is basing his opinion on some historical data and there is logic behind his expectations. Here’s a link to that just in case you’re interested in that scenario’s rationale. I get to the question to Jordan on that around the 6 min and 5 sec mark.

And don’t forget those who thought even one hike was nothing but a bluff and couldn’t happen. Stephanie Pomboy was already taking victory laps on Twitter before she ended up with egg on her face.

This is embarrassing (be sure to read the clueless comments below her post including Dave Kranzler’s “one at most – one and done” lol!!!):

https://twitter.com/spomboy/status/1496140354155950093?lang=en

True. There were a number of folks that thought they’d never hike or it would be a one and done. I actually had Dave Kranzler on the show a few months back and he mentioned they’d do 1 or 2 hikes and then wouldn’t be able to go much further with it. I may reach back out to Dave and get his reaction now after the Fed has already hiked 3 times, and with plans for a 4th and 5th hike in July and September.

There was also a whole other group of people that conceded there’d be hikes but that they’d be 25 basis point hikes and that we’d not see any 50 basis points hikes, much less 75 basis point hikes.

Clearly there are going to be a lot of surprised investors when this rate hiking cycle runs it’s course on all sides, and it is very difficult to know how much further to the upside they’ll be able to take things.

Good to see someone took GSV out of their misery. Truly epic management fail (old mgmt and Board).

Fact of the matter is we’ve been in a recession since 2007, supersaturated in liquidity and fudged all the stats to fool 95% of the public.