Ryepatch Gold reports Q2 financial results.

- Poured first gold from the new South Heap Leach Pad at the end of April 2017;

- Completed phase one of the new leach pad with ore stacking on portion 1B ongoing;

- Stacked 560,000 tons of ore during Q2;

- Improved strip ratio from 2.80:1 in Q1 to 1.25:1 in Q2;

- Increased crusher through-put, with crusher out-performing plan by 20 to 40 percent;

- Improved availability and utilization of the haulage fleet;

- Increased carbon plant efficiencies after rebuilding kiln and replacing acid wash plant;

- Mined and processed ore grades within five to 10 percent of modelled tons and grade;

- Completed leach pad audit which showed gold recovery within one percent of modelled recoveries;

- Recruited mine operators and technical staff to build workforce to near 100 percent capacity;

- Sold 100 percent of gold produced into the forward sales contract at $1,275 per ounce of gold, and;

- Purchased four 785C haulage trucks for $3.67 million, augmenting the current fleet and enabling planned production increases.

- At the end of the period the Company had cash and cash equivalents of Cdn.$22 million and had drawn down Cdn.$28.9 million of its credit facility.

VANCOUVER, British Columbia, Aug. 24, 2017 (GLOBE NEWSWIRE) — Novo Resources Corp. (“Novo” or the “Company”) (TSX-V:NVO) (OTCQX:NSRPF) announces that it has learned of certain recent public media disparaging one of the Company’s joint venture partners, Artemis Resources Limited (“Artemis”), and its Chairman, Mr. David Lenigas. Novo wishes to make clear that it does not condone such views. Novo and Artemis have recently completed definitive earn-in and joint venture agreements to explore for conglomeratic paleo-alluvial gold across Artemis’ land holdings in the Karratha region including the Purdy’s Reward prospect where Novo and Artemis recently announced the discovery of high grade gold mineralization in a bulk sample. Novo is currently gearing up plans for exploration and is looking forward to moving this new gold discovery forward.

Rye patch delivered a solid quarter for a company in a ramp up period in my opinion. Maintains a healthy balance sheet and was able to use its available leavers to turn in a good p&l statement. Outlooks of activities looks promising as well with additional hauling equipment and drilling plans. Anyone comment on what the market did not like from this report as stock is down ~5%.

They look to be doing all the right activity Imtiaz. Yes the additional hauling equipment should help the cause. The market will be watching their quarter over quarter results to see how things ramp up with production, and the re-rating process will begin. I agree though, it’s puzzling what’s holding back RPM considering how constructive that report of quarterly achievements is.

The market continues to be unimpressed with Rye Patch. The price action of this highly touted & pumped stock’s price action reminds me of the path Premium Exploration took after similar pumping. One direction – DOWM!

DOWM = DOWN

Clark (What?) Premium Exploration was a failed explorer in Idaho, where as Rye Patch is now a Gold Producer in Nevada. They couldn’t be more apples and oranges.

I’ve been following them since they were staking land in Nevada and were in a legal battle with $CDE Coeur. People doubted their resolve then and jumped ship, and claimed they were going down, but they won that case (as they should have) – giving them the Net Smelter #Royalty that they used to build up the company.

Next they continued to beef up #exploration and #development at Lincoln Hill and Wilco using that royalty stream, bought up a large land package around their other assets, bought back some shares of their stock, and just recently sold back to ramp up their #Production at Florida Canyon mine.

Critics moan on and on about their high share count, but if this was a beloved Canadian miner led by some “Mr-Important”, then even with that share count they’d be trading many multiples higher.

The have moved from #explorer to #developer to #producer in a few years and they will be able to capitalize on the ensuing Gold uptrend over the next few years…not still burn through money out hunting for an economic deposit like 99% of companies being touted (like Premium Exploration).

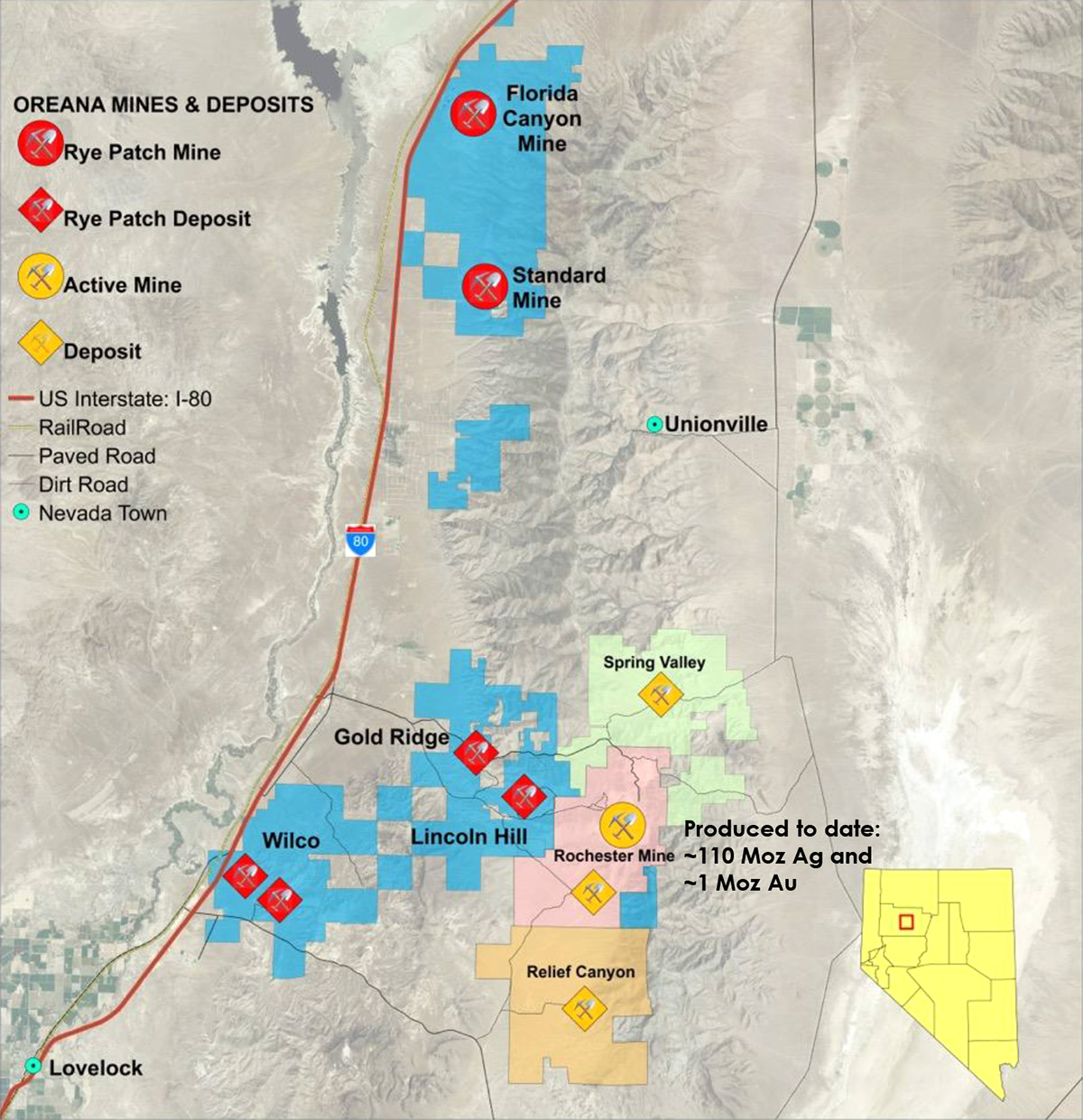

RPM has a district scale land package and will be feeding Florida Canyon with their resources from ~LincolnHill and ~Wilco next. That’s the whole reason they bought it, and I’ve seen a few haters only focus on Florida Canyon’s life expectancy and miss the whole strategy completely.

Here’s a #MAP that really puts things into perspective on the Rye Patch land package.

https://www.caesarsreport.com/wp-content/uploads/Florida-Canyon-Oreana-Gold-Tren.jpg

{kind=link}

(RPM) (RPMGF) Rye Patch Gold Presents At John Tumazos Very Independent Research Metals Conference

Aug. 7, 2017 – Corporate Presentation Slideshow#Gold #Production #Nevada

Excelsior:

Thanks for your comments and insights. RPMGF was at $0.23 at 12/31/16 and is down approximately 30% year-to date despite gold being up 12%+. I’m not suggestion Rye Patch is a failed explorer, but the price action trend speaks volumes.

Yes, the price action has been terrible, but Otto and some on Seeking Alpha goons launched trash-talking campaigns against RPM pretty hard, and people are more skittish than warranted. They are producing gold at a reasonable cost basis in Nevada, and have 2 feeder pits in Licoln Hill and Wilco. They are still very misunderstood as a company, and they have been for last 2 years. They were never valued correctly for having that Net Smelter Royalty either.

If you look at many producers 2017 has not been a rosy year, with most selling down significantly after the Q1 Run. Rye Patch looks par for the course in those respects. Most of the companies that have turned up were Exploration Discovery stories, not the producers.

I do agree with you that with the metals up, the miners performance has been lackluster and they are need of a fair bit of catch up.

I might be insane (well that’s a given) but this company is overdue for a re-rating higher, and believe it will come after they put another 1-2 quarters of production numbers on the books and maybe do a bit more exploration around their mine and at Lincoln Hill and Wilco to keep feeding the mill with those deposits.

That was not worded well. For clarity the exploration around Florida Canyon would extend that mine life, but the further Exploration and Development work at Lincoln Hill and Wilco will be 2 future pits that can feed Florida Canyon.

They also have other development projects beyond that, like Garden Gate Pass, building the future pipeline of projects.

Big Al likes Rye Patch and that’s all we need to know. Buy!

Osisko Mining drills four m of 36.7 g/t Au at Windfall

2017-08-24 16:20 ET – News Release