Ryepatch Gold strengthens cash position.

|

|||||||||||||||||||||||

|

|||||||||||||||||||||||

Integra was acquired with their main asset with a PEA showing a potential for 123,000 ounces per year over a 10 year mine life for $530 million. Rye patch ramping up to commercial production at half the Integra ounces per year along with other significant resource opportunities worth one quarter of Integra. Integra PEA shows a cost of $86/tonne cad, anyone know how Rye Patch compares? Could Rye Parch also be acquired as gold rebounds?

Thoughts?

Imtiaz Rahmat – Rye Patch as a producer at Florida Canyon, with development assets like Lincoln Hill & Wilco in Nevada has been severely undervalued relative to their peers, but is hard to compare with Integra, which was still just an advanced Development-stage project in Quebec. So one is already a producer and the other got acquired before going into production. The other factor is the Canadian bias where Canucks like to bid up companies in Canada to a premium valuation.

Rye Patch has never really been understood. First of all they were punished far too hard when going up against Coeur in their legal dispute over the land they staked, and yet, when they won that case and got the Net Smelter Royalty from Coeur, the market shrugged it off, and it has paid the company many multiple millions since it is has been in place.

The market recognize the value of the NSR which allowed them to buy up much of the adjacent land to their other projects, buy back a small amount of their stock, handle operations without constantly going back to the marketplace for dilutive capital raises, and to continue developing Lincoln Hill, Wilco, and Garden Gate Pass. If a Canadian company with some highfalutin promoters was behind that story the company would have been trading at 2-3 times it’s current valuation.

Now that Rye Patch has even taken things to the next level from Explorer, to Developer, to Producer, it is like the market isn’t even aware of it or all the success they’ve had. As a result, (RPM) (RPMGF) remains substantially undervalued as a new producer.

Even this news above of selling the Royalty back to Coeur for a 5 million payment which forward pays much of what they would have received over the next year or so was a brilliant way to raise capital without destroying the shareholder value through dilution, and hardly anybody seemed to notice.

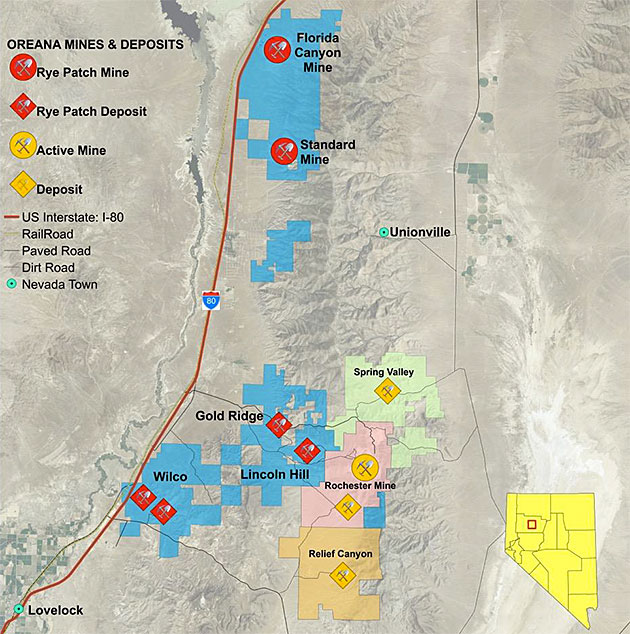

Rye Patch is developing a district size operation and eventually will get it’s due, but my only concern is that they get acquired before they finally get the chance to spread their wings. Coeur could actually be the suitor…..

** Check out this map which shows their projects and proximity to Coeur’s Rochester mine. I could see Coeur deciding to swallow up that whole area under it’s umbrella, but it would be best for current shareholders if they waited for Rye Patch to get re-rated by the marketplace first.

{kind=link}

Rye Patch Gold Corp. – Industrial Alliance Securities

Commissioning Progressing Well In Spite Of The Weather

George Topping & Alex MacIssac

(5 page report on Rye Patch Gold)

https://www.docdroid.net/PMH7Le6/rye-patch-gold-corp-industrial-alliance-securities.pdf.html

Congrats to Bill and the Rye Patch team. Another well executed transaction.