Gold stuck in limbo with the US economy continuing to struggle

Click download link to listen on this device: Download Show

Last week was dominated by political headlines that shook markets on Wednesday then immediately subsided. When political events move the markets it is crucial to determine if anything really has changed. Far too often these 1 to 2 day moves are simply blips on a longer term chart.

This weekend’s show focuses on hard data for the US economy and the main drivers in the gold price. Even though gold garnered a buy on Wednesday and has stayed above the $1,200 mark it remains in “no man’s land” as George Gero says in segment 7. We have some great guests sharing their opinions this week but we also love hearing from you. Please weigh in on the comment section and send me emails regarding companies and topics that you want to see on future shows – Fleck[at]kereport.com

- Segment 1 & 2: Kicking off the first two segments I have Dan Oiliver the Founder or Myrmikan Capital based in New York. We discuss the history of credit cycles and where the US is currently. In the second segment we look at the gold market and what could drive prices in the future.

- Segment 3: Valentin Schmid, Business Editor of the Epoch Times weighs in on the fact that the US economy has not improved.

- Segment 4: Adrian Day, Founder of Adrian Day Asset Management shares his views on how to invest when interest rates are rising.

- Segment 5 & 6: Rick Rule joins me for the first two segment of the second hour. We discuss the change in central bank policies around the world and how this will impact the precious metals and other resources.

- Segment 7: George Gero, Managing Partner at RBC Wealth Management updates up on the open interest in gold and why he does not like the fear trade driving the gold price.

- Segment 8: Brien Lundin wraps up our show further discussing the fear trade into gold recently.

Click download link to listen on this device: Download Show

Click download link to listen on this device: Download Show

Click download link to listen on this device: Download Show

Click download link to listen on this device: Download Show

Click download link to listen on this device: Download Show

Click download link to listen on this device: Download Show

Click download link to listen on this device: Download Show

Click download link to listen on this device: Download Show

And now for something completely different:

I’m not sure sucking $20 Trillion out of the general public would work, but it is a novel idea. I wonder how much China and Russia would buy.

A Massive Detour On The Road To Inflation

Mar. 24, 2017 – William Koldus, CFA, CAIA

[there are some good charts of the US Dollar, S&P 500, China vs TLT, etc… at the bottom. The top discusses inflation and deflation]

http://seekingalpha.com/article/4057799-massive-detour-road-inflation?ifp=0

US Treasury debt $19,846,001.52 million USD divided by the alleged 261m oz official gold reserves =$76,038.32/ oz

Current market prices for gold are a politically correct fiction and a lie.

good one Steve………..you are correct on the fiction and lie…….

If facts are important to this idiot, he should know that gold was not $27/oz in 1868. It was $20.67/oz. So gold has done a good job of protecting us from inflation, but not nearly as good a job as Standard Oil stock.

Hey CFS, I saw that quote as well. I can’t believe someone would say that and think it makes sense.

Thanks as always fella’s,

Much appreciated.

Cheers.

Thanks guys. Looks a really good line up this weekend. Looking forward to it.

Santacruz Silver Reports 2016 Annual Production Results and 2017 Update

March 24, 2017

“The Company produced a total of 970,332 silver equivalent ounces(1) in fiscal 2016, including fourth quarter production of 242,048 silver equivalent ounces(1) from its two operating projects. Production levels for the fourth quarter of 2016 were impacted by ongoing development and optimization activities at both the Rosario and Veta Grande projects which may allow for increased production levels in 2017.”

“We are excited to see the results of our efforts over these past months coming to fruition with an anticipated production increase in fiscal 2017,” stated Arturo Préstamo, Santacruz’s President and CEO. “This expected increase in production will be the result of significant development work completed at the Veta Grande and Rosario projects in the fourth quarter of 2016, which has set the stage for more robust 2017 operations. Although our focus on these development activities had the effect of reducing our fourth quarter 2016 production total, I am pleased to advise that the Company is now well positioned to steadily advance our production levels throughout the year.”

http://www.santacruzsilver.com/s/news_releases.asp?ReportID=783863

Technicals for Gold Miners Remain Weak

03/25/2017 | Jordan Roy-Byrne CMT, MFTA

“Last week we wrote that precious metals should see upside follow through but to be wary of the 200-day moving averages and February highs before becoming excited. The metals did follow through as Gold gained 1.5% and Silver gained 1.9% (for the week) but the miners disappointed. GDX gained only 1.1% while GDXJ finished in the red as did junior silver companies (SILJ). As spring beckons, the gold stocks are showing relative and internal weakness.”

“Two signs of weakness in the miners are visible in the weekly candle charts below. First, while Gold has already rallied back to its high the first week of February, GDX and GDXJ are down 11% and 15% respectively. The miners and the metals will not always be perfectly aligned but that is a rather stark divergence. Secondly, although Gold closed at the highs of the week in each of the past two weeks the miners failed to hold their gains. This is not exactly the type of price action that inspires more gains in the short term…”

https://thedailygold.com/technicals-for-gold-miners-remain-weak/

Silver Miners’ Q4’16 Fundamentals

Adam Hamilton – Mar 24, 2017

“The silver miners’ stocks have had a roller-coaster ride of a year so far. They surged, plunged, and then started surging again last week on a less-hawkish-than-expected Fed. Such big volatility has spawned similar outsized swings in sentiment, distorting investors’ perceptions of major silver miners. But their recently-reported fourth-quarter operating and financial results reveal the true underlying fundamental realities.”

As scarce as silver-heavy deposits supporting primary silver mines are, primary silver minersare even rarer. Since silver is so much less valuable than gold, most silver miners need multiple mines in order to generate sufficient cash flows. These often include non-primary-silver ones, usually gold. More and more traditional elite silver miners are aggressively bolstering their gold production, often at silver’s expense.”

“So the universe of majorsilver miners is pretty small, and their purity is shrinking. The definitive list of these companies to analyze comes from the most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. This week its net assets are running 5.4x greater than its next-largest competitor’s, so SIL really dominates this space. With ETF investing now the norm, SIL is a boon for its component miners…”

http://www.321gold.com/editorials/hamilton/hamilton032417.html

If you jump to the [55 mins 45 seconds mark] on this Video from the Swiss Mining Institute, then you’ll come to the (KS) (KLSVF) Klondike Silver Corporate Presentation. I find this to be an interesting Silver Development/Exploration story underway. (thanks again to JohnK for bringing it up here on the KER):

Mexus Gold CEO, Paul Thompson, Says Mines Are Ready To Produce Gold

Jasyn Blair Interviews Paul Thompson, CEO of Mexus Gold US (MXSG), and they discuss project updates and the beginning of Gold Production for one of their properties.

https://upticknewswire.com/mexus-gold-ceo-paul-thompson-says-mines-ready-produce-gold/

Thanks for posting……..I have a starter position at 10 cents & would like to buy more. Just don’t know how high to bid for it?

I got in at 1/3 of a penny and have traded in and out of portions of my position a number of times, but have a free ride core position in place at this point with it trading at 13 pennies.

Mexus will continue to surprise the marketplace, because investors just don’t understand how their JV with MarMar works, and how it allowed them to go into production with proven operators of Major mines, with almost no debt. It is the essence of true synergistic partnership. As a result they skipped 90% of the BS that mining companies do as explorers and developers and went straight into action mode. By 2018 the market will be aware of just how large of a production profile Mexus has, and maybe they’ll throw the Canadians a bone and get a venture listing.

One of the biggest drivers is that at San Rafael is about to be producing Gold & Silver. if you followed Paul’s timeline on that Pad 1 (it should be producing in the next 15 days). Then they are moving over to Pad 2 that should be producing by the end of April. Then they have Pads 3 & 4 cued up for the later in the year.

The next driver is San Felix that will be going into production on that heap leach pads later in the year, and both of these mines will be ramping up into a nice sized mining company by 2018.

Lastly, they’re 3rd property has about 2-3 main targets like Ocho Hermano and El Scorpio that will be interesting to see them keep exploring.

This link that (MXSG) just provided on their main website is a repost of and earlier release from last year that goes over the history & experience of their very capable JV partner MarMar holdings.

I’m very happy they finally have that posted on their website, as most investors will not realize that MarMar has been an operator on a number of successful projects and has provided all the equipment for the mining and milling.

http://cdn.ceo.ca/1cddtg2-History%20of%20MarMar%20Holdings.pdf

Wow, thanks for all the info Ex. I think it was because of a post of yours that I bought it. I know someone here was buying on the last pull back with the delay of start up at about 9 cents. I will be picking up some more ………..

Always glad to share ideas on interesting opportunities, but encouraging investors to always do their own research and due diligence and share any other opportunities they come across that may be worth reviewing.

Personally, I like to bring up stories that are unique, or overlooked, or maybe household names but where something significant is going on, just to see what others here think from a technical or fundamental standpoint. Sometimes like to bring up companies just to meet and chat with fellow shareholders. Investing is lonely and often I feel crazy for holding the companies I do, but feel a little less bonkers when other investors also see value in a company. However, I also have found my share of duds just like anyone else, and just work on getting more right than wrong.

I’m very interested in the success of Mexus, and that they really are putting not just 1 but now 2 mines into production (San Rafael and San Felix). MarMar is an experienced operator as their JV partners, so it seems like a good emerging Mexican producer. The fact that they achieved all this with hardly any debt is very impressive to me. While I like Mexico as a jurisdiction, it’s had challenges in certain parts of the county in years gone by, but still if you want Gold and Silver and its a great place to do mining.

Mexus has been one of my largest percentage increases in any mining company, but I didn’t keep my initial position intact all the way up. I’ve sold portions of it on the way up until I had a free ride position and then some…. In addition, I have added & traded a number of times in the $.09-$.12 zone, for a few swing trade profits but am basically just in to see how this transition over into production unfolds. Personally, I have nothing to really lose on my position in Mexus, but I do believe that putting 2 mines into production is worthy of a re-rating by the marketplace.

Everyone’s investing journey is unique to them, and should be a result of deciding what is best for you and your investing timelines and objectives. Mining companies of all stripes have no shortage of challenges that can befal them. Investors should always do their own due diligence and decide for themselves if they see value that is worth the risk.

Cheers!!

Good comments on Mexus guys! I will reach out to Paul and have him eon the show, IT is an interesting story but not many people I chat with are following it. The non-Canadian listing doesn’t help.

Thanks Cory, it is a good time to get an update from Paul as they are finally making it into Production. Always an exciting milestone for any mining company, as it is when they transition from burning money to generating revenues.

Yes, not having a Canadian listing doesn’t help with awareness up north, but Canadians get a little to nationalistic in their investing preferences and need to realize its a big world out there and not all resource companies are based in Canada 🙂

Aura Minerals Announces Fourth Quarter and Year End 2016 Financial and Operating Results and 2017 Guidance

(Marketwired – March 24, 2017) – Aura Minerals Inc. (ORA) (ARMZF)

Highlights:

> Gold production for the fourth quarter and year ended December 31, 2016 was 29,145 ounces and 122,760 oz, respectively

> Cash cost per oz of gold produced1 for the fourth quarter and year ended December 31, 2016 was $847 per oz and $846 per oz, respectively

> Income of $20,353 or $0.62 per share for the fourth quarter of 2016 compared to a loss of $11,886 or $0.42 per share for the same period in 2015. Income for the year ended December 31, 2016 of $19,020 or $0.64 per share compared to a loss of $14,479 or $0.56 per share for the same period in 2015

> A non-recurring gain on acquisition from Ernesto /Pau-a-Pique (“EPP Project”) of $19,886 (before tax) is included in the income for the fourth quarter and year ended December 31, 2016

> On June 23, 2016, the Company completed the acquisition of asset and liabilities of the EPP Project from Serra da Borda Mineração e Metalurgia S.A., a company affiliated with Yamana Gold Inc. for a total consideration of $9,597.

> During 2016, the Company announced the results from the NI 43-101 Feasibility Study for the EPP Project. Highlights include an average gold production of 41,000 oz per year over approximately 5.8 years, an initial CAPEX requirement of approximately $17,300 (partially funded by the Yamana Debt Facility), including working capital and contingency, a net present value at 5% after tax of $39,500, and an internal rate of return of 77%. Subsequent to the year ended December 31, 2016, the Company filed the NI 43-101 Feasibility Study for the EPP Project”

The #WestAfrica #Gold scene as it is continuing to consolidate.

For those that have been following along with the Yuge merger between $ACA.L Acacia Mining and $EDV Endeavour mining ……. The merger was called off (due to the export ban in #Tanzania being a major road block for Acacia Mining). This transaction not happening really changed the batting order of who may get acquired next by both of those companies as they move to diversify into different #development stage and #exploration stage companies, or other small to mid-size #gold #producers.

First, I’d also bring up that $IAG $IMG Iamgold is tied up in their merger with $MXI Merrex gold at present, so they are likely going to sit this one out.

When that news broke, the first 2 companies I thought of were $TGZ Teranga and $PRU $PRU.AX Perseus as potential new acquisitions for $EDV or $ACA.L to get their production profiles expanded immediately.

Perseus is more in debt and encumbered with poor operational results at current gold prices, and is still a bit tied up with their Amara acquisition.

$TGZ is solid, and really cheap at present, so if either of the big boys grabbed the next logical mid-tier it would likely be Teranga.

However, the next thought I had after reading the deal fell through, was that $SWA Sarama or $SCA may get aquired by $TGZ to consolidate the #SouthHoundeBelt and compliment their Golden Hill project. In that recent $TGZ video posted from the #SwissMiningInstitute conference, they unpacked their increased efficiencies at Sabadola, their ramp of #development at #Banfora and then they went through their 3 other main #Exploration targets. Clearly, Golden Hill is the one they are putting their focus on, so it could make good strategic sense for them to acquire $SWA or $SCA to lock down more property in that area.

It wouldn’t be fair not to mention that $ROG Roxgold is also right there in the thick of the action in the South Hounde Belt and could also be a wildcard acquisition for $ACA.L or $EDV, or $ROG could surprise us all and be the company that does the acquiring of $SWA or $SCA.

Another thought I had recently is that since $SCA is a Ross Beaty company and so is $ORG Orca Gold, I also wouldn’t rule out those 2 being consolidated in his #Africa land grab.

We haven’t discussed $AKG Asanko or $SMF Semafo yet either, but they also may do some acquiring or $AKG may also get acquired by $EDV or $ACA.L. I’m actually surprised no other companies have made a move on $AKG or $ROG yet, and this brings up the point that there is also room for another large #Major or #MidTier Gold #Producer to decide to diversify into #WestAfrica and get in on the action. (I would NOT rule out a market surprise from another Senior miner coming in and locking up some of these projects).

Lastly, it is important to bring up some of the MOST LIKELY candidates for #takeover or #takeout in #WestAfrica – those being:

1) $HUM.L – Hummingbird Resources

2) $AVK – Avnel Gold

3) $ORE – Orezone.

Since the deal with $EDV and $ACA.L is off the table, I could see both of those larger companies going after one of these 3 #Developers who are so much closer to #production than the earlier stage #Explorers.

*** This is definitely going to be an exciting 1-2 years in West Africa where we’ll likely see the number of companies consolidated down substantially in an #acquisition frenzy. Bring it !!!

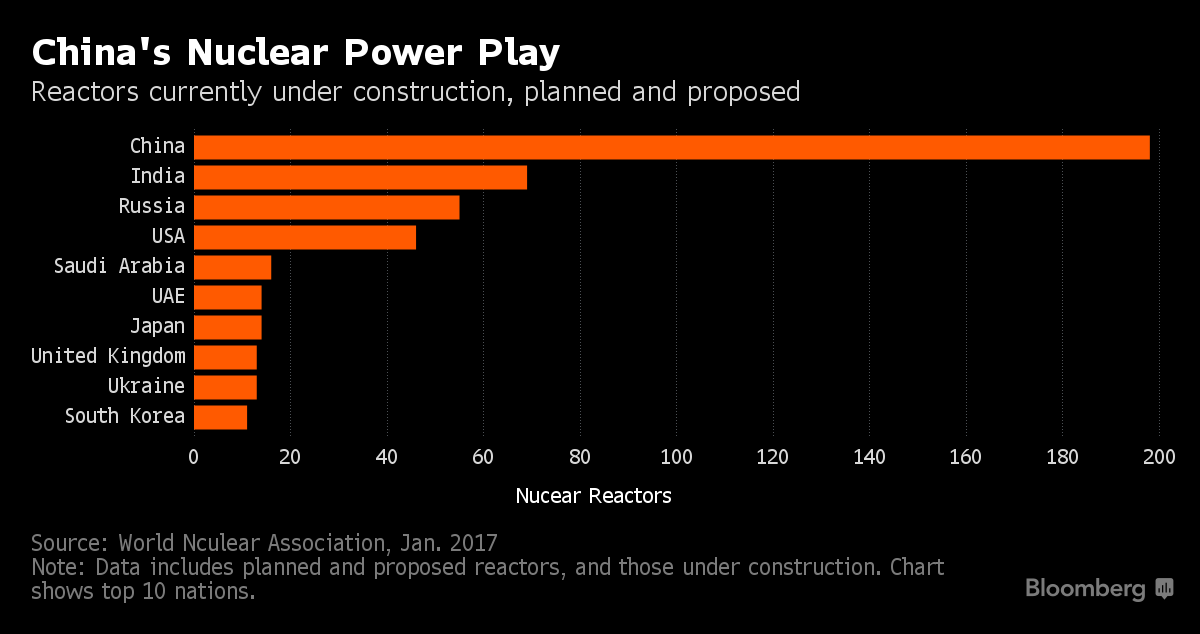

This chart of Nuclear reactors under construction, planned, or proposed may cheer up some Uranium mining investors:

https://assets.bwbx.io/images/users/iqjWHBFdfxIU/icT1_hHLtP5M/v1/-1x-1.png

{kind=link}

Ex:

So……….maybe 475 plants under construction or in planning stage…..I wonder what the yearly completion would be. Hard to take the graph and put a time element to it in order to gauge demand for fuel. Any ideas?

There are other sites I’ve posted in the past that actually put a timeline on each country, (for example I believe China has 60 more reactors that will be built by 2030, but over 200 planned and proposed). If memory serves the UAE has 4 reactors being built that will come on line in the next 3-5 years. I’d have to go dig those up pieces up by searching for the past posts.

The other thing to consider are that many of the newer generation reactors are larger and longer life and take 3-4 times the fuel of many of the older reactors in the global fleet. So the takeaway I got was that there would be much more demand on the planet as the energy needs without carbon emissions continue to expand.

This article by Leni is really good about 1/2 way down describing the different countries Uranium output from miners, the nuclear industry energy output by country, the different types of nuclear reactors and the overall demand side of the equation moving forward:

____________________________________________________________________________

Introduction to the Nuclear Fuel Cycle – Part 1 of 4

by @Leni on September 20, 2016

https://ceo.ca/@leni/introduction-to-the-nuclear-fuel-cycle-part-1-of-4

OK – This is Leni’s piece that really goes over the Supply/Demand side of the equation in the Nuclear Energy and Uranium Mining space. A great article!

The Uranium Supply Story – Part 2 of 4

by @Leni on September 29, 2016

This is one of the better overviews of North American Uranium Producers that I’ve come across.

_________________________________________________________________________

North American Uranium Producers

December 20, 2016 – Brian @ Junior Stock Review

http://www.juniorstockreview.com/2016/12/20/north-american-uranium-producers/

Top 10 Nuclear Generating Countries

World Nuclear Generation and Capacity – Data is from total 444 Reactors

(Non-US) World Nuclear Power Plants in Operation

Nuclear Units Under Construction Worldwide – Total (63)

Wow….a couple hours reading to get on top of the subject. Thanks Ex. for all that time you must have spent looking up and posting these articles. I never, never expect that much when I happen to ask a question.

Silverdollar – It is fun to share information with like-minded investors here on the KER. I’d already done most of that reading and research in the past and spent the time, so it was good to recirculate the data, as the Uranium market is much more opaque than the Gold & Silver markets and not very widely followed and misunderstood.

As a result, there is often a lot of calls for Uranium market to be over due to solar & wind, or cheap oil, and other garbage stories like that. The other thing that seems to happen every week is that because of something good or bad that happens at just 1 plant, people draw up sweeping generalization about the entire sector and are usually way out of the touch with the actual facts.

Sometimes it is best to lay out the big macro fundamental picture and see how this energy commodity will be trending over the next few years.

Energy…. gotta have it or we can’t access the KER 🙂

Prepare to Profit Series Part 3 – (Uranium)

A Huge Part of the Russia/Trump Story Nobody is Talking About

Katusa Research – JANUARY 25, 2017

“The U.S. gets a little uranium from its rapidly-declining stockpile of decommissioned nuclear warheads, a little from Canada, and a little from Australia.

But the U.S. gets the bulk of its uranium (more than 50%) from unfriendly, Russia-influenced sources.

This is a dangerous positon for the United States. Over the past decade, Russia and the United States have gotten into a variety of low-level disagreements. They have one currently in Syria.

If a disagreement were to escalate, Vladimir Putin could easily “play the uranium card” and cut off Russian uranium supplies to the United States. Putin could also exert influence over Kazakhstan and block uranium shipments to the U.S. This would cause an American power crisis.

The U.S. cannot rely on big producers like Canada and Australia for uranium imports. Neither country can supply enough uranium to fulfil American demand. More importantly, both Canada and Australia have signed long term agreements with India and China. This means there is even less uranium available for U.S. imports.

Raw, physical uranium is of no use to nuclear power producers. It must be refined or “enriched” to a specific grade to be of use. This refinement process is extremely expensive, extremely difficult, and extremely time consuming. In the uranium market, enrichment capacity is even more important than raw, physical uranium supply.

Russia controls over 50% of the world’s uranium enrichment capacity. The enrichment facilities in the U.S. and in countries friendly to the U.S. are running virtually flat out.

A trillion pounds of uranium could magically appear in the U.S., and couldn’t be used to produce power because the U.S. doesn’t possess or have access to the needed enrichment capacity. Building this capacity would take more than 10 years.

The U.S. cannot simply “flip a switch” and get its electricity from other power sources like dirty coal, solar, wind, or natural gas. It does not have the infrastructure to do so. Building it would take a decade…..”

https://katusaresearch.com/prepare-profit-series-part-3-huge-part-russiatrump-story-nobody-talking/

UEC’s Amir Adnani with the Mercenary Geologist, Mickey Fulp at the PDAC in Toronto…

Mar 22, 2017

(AXY( (MGMXF) Alterra Power Corporation’s CEO John Carson on Q4 2016 Results – Earnings Call Transcript

Mar. 16, 2017 – #RenewableEnergy

“I saw 2016 as a transition year, I see 2017 as a real year of liftoff. We’ve built a great sustainable base. We now have eight operating plants in #wind, #hydro, #solar and #geothermal power. As far as I know, we’re the only #CleanEnergy company in the world with operations and management expertise in all four true clean energy technologies. And from this base, we plan to at least double our size over the next few years. I say at least double because quite frankly, we have projects in our pipeline that could triple our current size by 2020, and we have the human resources and access to capital to execute this amazing growth platform. That’s why I can say that I’m as excited about our future as I’ve ever been since beginning the company in 2008.”

—- Ross Beaty

Rick Rule Pre PDAC 2017 Mining Stocks on BNN Market Call – http://www.pennyminingstocks.com/rick-rule-pre-pdac-2017-mining-stocks-bnn-market-call/

Thanks Anon. That was a great Rick Rule interview (from a few weeks back) and covered a number of stocks like $IVN Ivanhoe, $ANF Anfield Gold, $KL Kirkland Lake, $CGP Cornerstone Capital & $SOLG.L SolGold, $PVG Pretium Resources, $NAK $NDM Northern Dynasty, the XAU Index, $DDC Dominion Diamond, Reservoir minerals/ $NSU Nevsun, $HL Hecla Mining, $PAAS Pan American Silver, the Silver market fundamentals, $CDB Cordoba, $SLW Silver Wheaton, $BGM Barkerville Goldmine, $VIT Victoria Gold, $DPM Dundee Precious Metals, $LUC Lucara Diamond, investing in #Gold bullion, Off balance sheet liabilities and #debt of the US Government, $TV Trevali Mining, $NXE Nexgen Energy, $ALS Altius Minerals, $BTG B2Gold

Rick Rule at PDAC 2017…”We’re about a third the way through this Bull Market”…

Mar 22, 2017

Rick Rule on stocks, oil, gold and silver, and the future of the markets //

David Moadel – Mar 22, 2017

“Rick Rule on stocks, oil, gold and silver, and the future of the markets // investing expert, investment tips, stock market collapse 2017, market crash 2017, recession coming, stock market collapse imminent today, stock market crash explained, when will the market crash, when will the stock market crash, stock market crash predictions, oil market crash, oil market collapse, bond market crash 2017”

Metals & Resources Market Mechanism Shifting: Unique Opportunities Now – Rick Rule Interview

CrushTheStreet – Mar 26, 2017

“The world’s top resource expert (and we’re not exaggerating) is back to give us some details on what he’s looking at and how he sees the resource sector as we end Q1 2017. An awesome opportunity is revealed toward the 2nd half of the interview in regards to Cobalt and political changes in the world.”

TOPICS IN THIS INTERVIEW

01:35 Gold Price Correction in Perspective

03:10 Vast Majority of Jr. Miners Valueless

04:15 Massive Capital is Flowing in = Bull

06:50 Current Cycle vs Past Cycles Rick’s Seen

09:20 Cobalt Trending; Battery Tech & Politics

13:20 Cobalt is leading a Commodity Boom

Tanks ANON !

Can’t really understand where price inflation would come from. Vehicle sales are falling along with prices, both new and used. Household debt is already high. Crude has moderated and fallen to mid-forties. Wages aren’t climbing steeply. Competition in groceries is supposedly dropping prices. Retailers can’t keep their doors open. Housing is healthy, but formation of households isn’t happening. 40% of 25-35 young people are living with parents because debt and crappy jobs don’t give them the income to strike out on their own. Can somebody enlighten me on the subject?

You bring up some good points SD. There is a lot to consider and I will keep this in mind. My initial comment would be there is that there is a lot of money tied up in the markets. If this money starts to flow into real goods that would drive prices much higher. Who knows maybe Rick will be right with his deflation call.

SD…has a lot of valid points………..jmho

China’s Economy Explodes In February 2017

China’s February 2017 power consumption exploded. I have never seen such a large spike.

This means that there is a high probability that China’s GDP growth will accelerate and this will bode well for commodities. We’ll keep monitoring this trend. Cont’d…

http://seekingalpha.com/instablog/839735-katchum/4971882-chinas-economy-explodes-february-2017?

I think the title is supposed to be “stuck” not “suck”

I sure how we don’t see a major Gold Suck…

Then we’d be Stuck in our positions…

That would, in fact, suck…..

Nobody likes finding out they are the sucker….

how = hope (but hope springs eternal….)

Thank PF. My fault on the title.

So for those that have the time, this is over a 4 hour video from the Swiss Mining Institute conference with a few different key note speakers and about a dozen company presentations made.

In particular I remain very impressed with (TGZ) Teranga Gold and their presentation that starts at (3 hours, 19 minutes, and 30 seconds) is super solid. The year that they unpack for the balance of 2017 looks like this is another company that could really get rerated in the second half of this year.

Are there any other Teranga investors out there with any thoughts?

________________________________________________________________________

Swiss Mining Institute – Geneva Conference 22 March 2017 (Morning)

Mar 22, 2017 – Mandarin Oriental – Geneva

This link to the Swiss Mining Institute is more helpful. You can see all the individual speakers or presentation down below and click on those directly, and the video up above will just play that segment.

I’ve been watching these this week from that youtube one, but realize this link would be better for jumping right to the actual talk you want to see.

Enjoy!

I apologize. That last post and link I included has videos from last year’s 2016 conference down below, so it would be much better just to watch the 4 1/2 hour video at the very top of the page or the original youtube link up above from March 22, 2017.

Sorry about the confusion, but definitely a lot to take in from the Swiss Mining Institute.

Rick Rule

http://palisaderadio.com/

Ali Zamani: Former Goldman Sachs Manager Says Gold And Gold Stocks Are Best Investment

By Collin Kettell – March 24, 2017

The Next Bull Market Move Interview – Collin Kettell, CEO & Partner, Palisade Global Investments Ltd

by @bullmarketmove on March 26, 2017

I think Collin nailed the bottom in Uranium in december 2016 but Rick Rule and John Kaiser has a point that its Japan who makes the next bull call in uranium and that is the restart of Japans reactors. Until the uranium price gets going the uranium producers will not move a lot but the uranium junior explorers could surprise to the upside.

I bought some Appia energy an uranium explorer that Palisade research was recommending. I bought it because of the uranium guru James Sykes is now in front of Appia energy and making the calls. They will have some initial drill results very soon maybe in April. James Sykes was involved in NexGens big exploration success. I hope he does it again with Appia Energy. Appia is for the long term investor I think.

Sadly there has just been a recent setback in the restart of the Japanese reactors with this latest news. This could be a setback for Japan, but Rick Rule and John Kaiser are over-emphasizing Japan’s role in the future, and are not even discussing the much more important role of China moving forward (not to mention the reactors in India, UAE, Turkey, S. Korea, and even the US that are being built or planned at present).

{Also — keep in mind the author of this piece is a Greenpeace wacked out Leftist, that seems very negative on Nuclear as preconceived prejudice and doesn’t seem to have a clue how much base load power that Nuclear handles versus Natural Gas plants or Solar Wind)

_________________________________________________________________________

Japan court shocks nuclear industry with liability ruling

“Court sends a shockwave through Japan’s nuclear establishment with ruling on Fukushima accident.”

By SHAUN BURNIE MARCH 20, 2017

http://www.atimes.com/article/japan-court-shocks-nuclear-industry-liability-ruling/

Blue – I have been following the success of Appia Energy recently as well, because as a Nexgen shareholder, I recognize the talent of their team and James Sykes in particular.

However, the main exploration company to follow in the Athabasca is still Nexgen,(who has a world class Tier 1 deposit in the works). Nexgen has clearly overshadowed Fission (with all of their water issues, failed merger with Denison, partial ownership by an Asian consortium, and the general mess they’ve created). If one does any homework on the water issues Cameco has had to deal with with freezing the ground to mine, and the water cave in, then they’ll quickly deduce how problematic Fission could be in comparison to Nexgen. To be clear, both companies may eventually get acquired but they are a LONG way from even being close to production in the next 5-10 years.

After Nexgen , Denison is still the clear leader in both exploration and development in the Athabasca (after Cameco & Areva). Besides the backing of the Lundin family, Denison has a 25% stake in Govi-Ex, they have an environmental remediation business throwing off revenues, and most importantly, they have been producers in previous cycles and have the skill sets to take their projects into production. It should also be noted that Denison owns over 20% of the mill with Areva that processes the Cameco ore from Cigar Lake, so they are currently Producers. With Cameco scaling back, it is most likely that Denison will fill that void at the mill with their own exploration and development pipeline.

Next up UEX Corp and ALX Uraniuim are two more of the most prolific Explorers in the Athabasca basin, and Canalaska has quite a substantial land package (although they’ve been derailed for the last year on that diamond side tangent). Also Skyharbour Resources is another Athabasca explorer kicking up some dust and is now gaining more traction with investors. Kivalliq has some exposure to a few different basins and has their Genesis project near the Athabasca.

There is definitely a lot going on with the Uranium explorers in Canada for sure.

While Canada gets much of the attention due to grade, it should be noted that US producers with the lower cost Insitu mining method are still far undervalued in comparison. Energy Fuels, Ur-Energy, and Peninsula Energy are all producing at much lower costs, with few water issues, and much less land disturbance than the Canadian explorers many are so fixated with.

Anfield Energy is about to be the newest member of this club with the US assets they bought off Uranium One and they will also be producing later this year utilizing the In-situ mining method. Lastly, Western Uranium is gearing up to be yet another insitu miner in the US, and are worth following.

Also, Australia has a number of projects under development like Toro Energy, Bannerman Resources, Boss Resources that have hardly been noticed by the marketplace yet. There still is Energy Resources of Australia as well, but I don’t like their company and they’ve made too many environmental blunders for me to feel comfortable with them

To round out the Uranium discussion there are the wildcard African producers and development stories held by some of the larger majors like Rio Tinto & Paladin, but also new (repackaged) stories like GoviEx and Deep Yellow. There is also Plateau Uranium developing their project in Peru, and a few other wildcard European deposits like Mawson or Greenland Minerals.

Lots to follow in the Uranium Sector.

John Williams on Greg Hunter:

https://www.youtube.com/watch?v=wYjH8013KiI

Hi Ex!

Thank’s a lot for your opinion and info regarding SLL the other day. I couldnt agree more that well run experienced Lithium companies is to prefer.I didnt pull the trigger this time.

Right now I have a lot of Tinka Resources shares, I believe like many others that zinc is the place to be and Tinka feels like a very good exploration company with a lot of positiv catalysts this year.

Here is a very informativ interview with John Kaiser about Zincs future and why its in a real bullmarket:

https://m.youtube.com/watch?v=n_tinZ01q5I

John Kaiser on Zinc:

https://m.youtube.com/watch?v=Ypxa9getXUg

A brand new Tinka presentation from 23/3.

https://www.tinkaresources.com/assets/docs/ppt/tinka-presentation-23-march-2017.pdf

Zinc price in a bull market:

(look at the 5 year chart)

Zinc supply down dramatically for several years

(look further down the charts):

http://www.kitcometals.com/charts/zinc_historical_large.html

Tinka ceo interview:

https://www.youtube.com/watch?v=n_tinZ01q5I

Brent Cook buying Tinka:

http://www.bnn.ca/investing/video/brent-cook-and-joe-mazumdar-discuss-tinka-resources~1072137

I looked att Arizona mining from the beginning of 2016 when the Zinc bull market started. Arizona was trading at 0,35cad when John Kaiser started the buying Arizona mining. It went to 3.48 cad late 2017. Tinka is at the same stage as Arizona mineral was one year ago. I know that this is Peru and it could be more risk with Tinka but you have to place your bets carefully. Peru is mining friendly and has good tradition in silver and zinc projects.

Zinc is in a great bullmarket and Tinka is in the beginning of its journey with a lot of potential and a lot of drilling . Zinc and Tinka has good momentum right know and Im gonna ride it this year into next year.

Zincs supply crunch is the best indicator of its great bullmarket.

Sorry if Im pushing zinc and Tinka to the moon but Im really excited and it feels really good when you find a market that doesnt trick you all the time. Im so used to golds bad up and downs and I think that next year when gold really has started to race to the next level in its bullmarket everybody is going to feel like how I feel about Zinc and Tinka,

over and out

Hi Blue – many great points in that post on Zinc. I couldn’t be more in agreement, and have been banging the Zinc drum for the last year every chance I get.

Yes, Tinka is a great exploration prospect, as is Vendetta Mining. I own both, but trimmed recently as they both have jumped up so far so fast, that they may be getting a bit too far ahead of themselves. That final leg up in Tinka was the Brent Cook/Joe Mazumdar effect, but they came in rather late in that move. Both Tinka and Vendetta do have drill projects going on later in the Spring that will be catalysts (to the up or down side moving forward). I’m excited to see how things go this year for both companies.

As for Arizona Mining, I’d say we nailed that one here on the KER way before almost anyone else (including John Kaiser) because of our wonderful contributor (Dan, calgary) that tipped us all off to Wildcat Silver back in the day. Over time Wildcat Silver reorganized as a “Zinc-focused” company versus the Silver, and was reincarnated at Arizona Mining. We covered that whole transition on here on the KER and I made some nice coin riding that one up, but bailed way too soon. I never imagined they’d have 10 drill rigs running simultaneously on that property, and they really did hit the mother lode in grade, but the consensus is from many geologist (and a few hit pieces from newsletter writers) that the Manganese contents are problematic at the smelters and smelter penalties really impact their economics. The other big challenge Arizona Mining has is that their land is surrounded by federal lands that they really need access to if they are going to have the room to set up their mine/mill/tailings and have enough room to expand to that project for the economies of scale to make it economic. The permitting on that is going to be difficult as that area has had some local push-back on new mines.

Also, there is the large Zinc project that Ivanhoe Mines has but it is their “throwaway property” as Rick Rule calls it, because most of their focus are the other 2 projects on Copper & PGMs.

While we’re reviewing Zinc companies let me throw out a few more companies to do some homework on:

1) Heron Resources – This is an Australian company with a large Zinc / Copper project and they’ve been held up trying to get their financing all squared away, and as a result have been sitting idle (not really participating in the recent Zinc rally). Once they get that financing in place though….. I believe this will be a great story to follow.

In addition, Heron has recently spun out their other Cobalt/Zinc/Silver projects into Ardea Resources, and that stock has gotten downright frothy from all the pumping on CEO and Hotcopper, and it is amazing that all those assets were inside of Heron Resources for years and nobody even noticed. Regardless, I wish Ardea all the success in the world (even though it is way ahead of itself) because Heron still holds a large number of shares in their company as the mother ship.

2) Foran Mining – This company has already had a huge move up over the last 12 months but their Zinc focused Base Metals project is turning out to be quite the story and shows a great deal of potential.

3) Callinex Mines – They were off to a great start and have defined a nice deposit thus far, but just had the stuffing knocked out of them last year when they missed on some wildcat drilling they were doing. In my opinion, the market completely over-reacted and tanked their share price. Recently, I’ve decided to be a buyer and anticipate much better exploration results in their 2017 drill program, and could see those assay results being a catalyst to put this explorer back on the map in a big way.

4) Canada Zinc Metals – This stock has a big following with the Canadian Zinc fanatics, and rightly so. They have larger resources than many of the Zinc explorers like Tinka and Vendetta, but haven’t had as dramatic of a price increase yet and have flat-lined for the last few months. Due to their proximity to Teck I see them being a potential acquisition target down the road.

5) Zazu Metals – They have a large Zinc/Lead project fairly well defined right next to Teck’s only active Zinc mine – Red Dog in Alaska. The Lundin family also have a large strategic investment in Zazu through their “Zebra Holdings” company. Obviously the marketplace is anticipating a takeover here, but recent info I’ve read by investors entrenched in the Zinc market feel this one may stay on the vine a while longer and get shelved. Who knows…?

6) Aquila Resources – They are Gold forward company, but happen to have very large Zinc resources as well, and the recent rise in Zinc has got investors chasing them from both sides of the story.

7) Thunderstruck is a large Zinc & Gold project in Fiji that has really moved recently and has newsletter coverage from Thom Calandra and many Aussie investors that also follow them.

8) Rathdowney Resources is making the rounds, but some feel their grade may not be adequate to make it worth the candle. I’m still doing more research on this one but felt it was worth mentioning.

9) Pasinex Resources is great up and coming Aussie run Zinc story that is operating in Turke of all place. They definitely have the jurisdiction risk, but have gotten much more attention lately as more Gold companies and have been breaking into Turkey’s resource markets.

10) InZinc – Mining is a big stock that John Kaiser and crew follow, and there seems to be a split between the lovers and haters of this project. I believe they have something real, but the storty has been over-hyped in comparison with their peers.

11) Constantine Metal – I’ve been a shareholder off and on with Constantine and they have a nice Zinc/Copper/Gold deposit that they can use gravity assist mining with and they’re building an access road. The challenge here is how much community push back there is due to Salmon spawning and a Bald Eagle mating area. I see these as being a larger problem than some are willing to admit (think Northern Dynasty), but their team and deposit is top notch.

12) Trevali Mining – I’d be remiss if we didn’t mention the go to Zinc Producer in Canada – (TV). They’ve had their challenges for sure, but they are actually producing Zinc, which is more than most Zinc miners can claim. Also, they really surprised the markets recently by picking up some old Glencore projects that are already producing properties. They really diluted existing shareholders is major way from the old assets, and now the marketplace is trying to find equilibrium on what the combined company with the new share count will be worth.

*Beside Trevali, most other Base Metals companies are not strictly Zinc focused but companies like Glencore, Hudbay, Teck, Nevsun, Nyrstar, Lundin Mining, and Vendanta do produce large amounts of the Zinc supply.

13) There are a few new Zinc names popping up that are more marketing fluff than substance at this point like Zinc One, Adventus Zinc, Darnley Bay, and Kootenay Zinc but many are near or on old resources, so their exploration should be followed closely to see how they start to tie some of these resources together as they work towards their resource estimates and economic studies.

14) There are about a dozen more Aussie Zinc & Base Metal stocks that I’m still reviewing like Alara, Aurelia, Consolidated Zinc, Golden Rim, Ironbark Zinc, Macphersons, Marindi, Metalicity, Metals Australia, Overland Resources, PNX Metals, Rox Resources, Terramin Australia, Variscan, and Venturex that show promise as well.

I Zinc 2017 is going to be a fun year in this sector !

We discussed this before, but the other area to really play the appreciation in Zinc prices is by investing in SILVER MINERS.

Most Silver companies also have Zinc & Lead credits, and in most cases, the marketplace is not properly projecting out how the rise in Zinc (and also the rise in Lead) prices are going to really help out the Silver producers costs and margins, and how they will assist the Silver development stories economics and Feasibility studies.

One way to hit 2 birds with one stone is to acquire Silver miners that have healthy Zinc exposure as well and take advantage of the recovering bull market in Precious Metals, and the upside pricing (due to many old mines shutting down and smelter demand for Zinc & Lead).

Fun times!

One more thought is that a 3rd way investors can play the Zinc price appreciation beyond the Zinc & Base Metals miners, and beyond the Silver miners with Zinc credits, is through some of the Prospect Generator companies like Eurasian Minerals, Strategic Metals, Globex, Avrupa, and Solitario Exploration that have exposure to Zinc but are diversified across a number of projects, commodities, and jurisdictions.

Trevali CEO discusses Glencore deal, Zinc markets

MATTHEW KEEVIL MARCH 27, 2017

http://www.northernminer.com/news/trevali-ceo-discusses-glencore-deal-zinc-markets/1003784876/

Callinex enlarges footprint in Flin Flon camp

TRISH SAYWELL MARCH 22, 2017

http://www.northernminer.com/news/callinex-enlarges-footprint-flin-flon-camp/1003784690/

I hear you, Ex!

I know you often is very early in finding good value in these tough resourcemarkets. Thats why I appreciate your opinion. My take on Zinc and other bullmarkets is that its not to late to enter into a bullmarket that has run for a while. Its often better to step in when its been proven that it is a bull than catching a falling knife. Its easier said than done. I really like your brief descriptions in every zincminer you brought up. I like bet big when I find something I believe in and right now it Zinc and Tinca🤗

Here is Mavens take on Zinc:

https://www.resourcemaven.ca/blog/zinc-strong-fundamentals-equity-options/

Good thoughts Blue, and thanks for the kind words. Yes, sometimes investing in the trend once it is established is a good thing (the Trend is your Friend…..until it isn’t…)

Tinka is a great little explorer in the Zinc space and widely followed over at ceo.ca.

Here is the Tinka room that you may find interesting if you scan back up through the old comments;

Blue – That was a good Zinc overview from Gwen Preston. Thanks for sharing it.

If memory serves she is promoting Kootenay Zinc at present, but was a fan of Vendetta in the past.

I think she has Darnley Bay in her portfolio of resource stocks.

I should have added Karmin Exploration in that list of Zinc companies up above as their Aripuanã Zinc Project is a big undeveloped asset, but their other 2 projects are Gold focused, so I forgot about mentioning them.

Very nice breakdown Ex and Blue. Thanks for your insights into Zinc and some Zinc companies!

This was the place to post it I guess.

New mine in Iran to add 800,000 tonnes of zinc concentrate every year

IMIDRO estimates the lead-zinc-silver mine has 154 million tonnes of proven reserves, which could rise to 700 million tonnes after exploration. Reuters notes the 800,000 tonnes of expected annual zinc concentrate compares to 13.2 million tonnes of ore with zinc content mined throughout the world last year.

Story is from mining.com

Thanks B!

Thanks b. I hadn’t heard of that Iran mine yet.

Always glad to discuss the Zinc miners. Lots of action in that space over the last 6-12 months.

doesnt surprise people not hearing of it.

They are the bad guys after all.

Resources in Iran are eye watering, just like Iraq and Afganistan, which is why they must be invaded of course.

Well, because Israel wants it,but the resources make it more palatable.

I thought that much zinc would be enough to affect supply, maybe the expected price explosion wont be so explosive.

Here’s.a fun one.

27 week movement in gold,silver,Dow and Russell.

Hit animate button on the right.

https://stockcharts.com/freecharts/rrg/?s=$GOLD,$SILVER,IWM,$DJX&b=$SPX&p=w&y=1&t=10&f=tail,d

Cory or Al, please help me out, my comment earlier today has been awaiting moderation a long time now.

It’s posted now Blue. Sorry for the delay.

FYI – Any comment with more than 1 link will get put into moderation.

Aha didn`t know that

Stateside Report Podcast – March 26, 2017

In this episode of the Stateside Report Podcast we take a look back at the week in gold, silver, the base metals and the stocks, we highlight a new TSX-V silver explorer that has an exciting risk-reward opportunity and then we talk about the press releases from the Canadian junior exploration companies for the past week including Genesis Metals, GIS, West Red Lake Gold RLG, Arizona Silver Exploration AZS, Ximen Mining XIM, Macarthur Minerals MMS, Enforcer Gold VEIN, Kootenay Zink ZNK, Tanzanian Royalty TNX, Columbus Gold CGT, Bonterra Resources BTR, Astorios Resources ASQ, Lumina Gold LUM, Mundoro Capital MUN, West African Resources WAF, Engold Mines EGM, Dios Exploration DOS, Black Iron BKI, Secova Metals SEK, Mariana Resources MARL, Nexgen Energy NXE, Vanstar Mining VSR, Canstar Resources ROX, Salazar Resources SRL, Altitude Resources ALI, Alset Energy ION. We talk gold, silver, copper, lead, zinc, iron ore, coal, uranium and oil.

Regarding GDXJ – Goldfinger had a nice seasonality post today:

@Goldfinger – “April is 2nd best month of the year for $GDXJ”

{kind=link}

@Goldfinger – “April is also a strong month for Gold:”

{kind=link}

Drama in DC

Gary Wagner – March 24, 2017 –

Weekend Review #TechnicalAnalysis #Video #Gold #Dollar

The Suspense is Killing me

by Fullgoldcrown @ 10:35 am – Goldtent TA Paradise

#TechnicalAnalysis $HUI #Chart

A Grinding #Gold Market: Key Trades

Morris Hubbartt – Super Force #PreciousMetals #Video #TechnicalAnalysis

Mar 24, 2017 (double click the various Blue Links to play the Video segments)

Monday’s Predicted Daily Price Trends for #Gold and #Silver

VantagePoint – Friday March 24, 2017

> Spot #Gold Intra-Day Trend: Higher. VantagePoint’s short-term indicators are bullish.

>Spot #Silver Intra-Day Trend: Higher. VantagePoint’s short-term indicators are bullish.

The silver-gold ratio (SLV:GLD) punched throught the 20, 50, and 200 day moving averages today and has stalled (so far) at pitchfork resistance…

http://stockcharts.com/h-sc/ui?s=SLV%3AGLD&p=D&yr=1&mn=1&dy=7&id=p59981133445&a=510416953

GLD jumped well above the pitchfork trigger line that originates at the February high. Let’s see if it pulls back to it tomorrow…

http://stockcharts.com/h-sc/ui?s=GLD&p=D&yr=1&mn=4&dy=0&id=p38983924215&a=513961902

PPP is looking good today as it has popped through fork resistance:

http://stockcharts.com/h-sc/ui?s=PPP&p=D&yr=0&mn=7&dy=13&id=p36054359233&a=507178767

Fork yeah!

The yen looks good but has run into resistance at the 30 week MA this morning:

http://stockcharts.com/h-sc/ui?s=%24XJY&p=W&yr=7&mn=3&dy=22&id=p82313585444&a=489358284

SLV jumped through fork resistance and a 50% Fibonacci fan resistance:

http://stockcharts.com/h-sc/ui?s=SLV&p=D&yr=0&mn=9&dy=9&id=p18499643546&a=511613782

The miners are doing poorly relative to silver (SLV is up 1.6% right now while SIL is up just .31%)…

http://stockcharts.com/h-sc/ui?s=SIL&p=W&yr=5&mn=10&dy=0&id=p92149973419&a=421379256

Terrible. I don’t see this turning unless a new low in the ratio is made. Once this pattern of underperformance is established, it usually means there is going to be a massive drop in the miners before they turn it around.

The miners and the Dow’s major pivots have more or less coincided with each other. I don’t think the miners can rally to new highs without the Dow rallying too.

GDXJ gapped up $1.00 today but has already filled 80 cents of it:

http://stockcharts.com/h-sc/ui?s=GDXJ&p=D&yr=1&mn=2&dy=13&id=p55254454058&a=511146714

I predicted that the dollar would perform poorly after the Fed’s rate hike and it has. It looks terrible (UUP):

http://stockcharts.com/h-sc/ui?s=UUP&p=D&yr=0&mn=9&dy=0&id=p85836308844

The move down is probably just getting started but there should be a bounce soon:

http://stockcharts.com/h-sc/ui?s=UUP&p=W&yr=2&mn=9&dy=0&id=p50780296246

Good call on the US Dollar post Fed rate hike and Fedbabble.

Some silver miners looking terrible so far today, with many putting in large black candles on a day silver is up substantially. EXK for example is poised on the edge of a cliff. New lows coming soon probably.

Silver’s pop today looks like nothing more than suckers rally so far. Need to see substantial improvement in the miners before the close for me to change my mind.

I think you’re too bearish, Spanky. The miners are doing relatively poorly, as I stated above, but the bearish implications of such a short term divergence are far from a foregone conclusion.

The huge gaps up today didn’t help and the futures and options calendar probably doesn’t either.

This type of underperformance reminds me of January 2016, at best (in which miners got an absolute beating before flipping on a dime and shooting up like a rocket), and at worst presages a 2008 type of meltdown in the stock market. The former is not something I would typically bet on. For the love of god can’t we just get a normally trending move in the miners? This consolidation in the miners definitely looks objectively worse in price and time and relative to very long term MAs than any other consolidation since 1999 (with the exception of 2008).

Silver is above the 50 and 200 week MAs and the 50 wMA will soon cross above the 200 wMA (that last happened in 2009). The following chart won’t update until this evening.

http://stockcharts.com/h-sc/ui?s=%24SILVER&p=W&yr=7&mn=5&dy=0&id=p87093418701&a=513709899

Nice!

EXK beautiful bear flag on the weekly chart. The only thing supporting it atm is the 100 WMA.

The lower weekly bolinger band is going to get tagged soon. That means EXK at 2.70 or lower.

New mine in Iran to add 800,000 tonnes of zinc concentrate every year

IMIDRO estimates the lead-zinc-silver mine has 154 million tonnes of proven reserves, which could rise to 700 million tonnes after exploration. Reuters notes the 800,000 tonnes of expected annual zinc concentrate compares to 13.2 million tonnes of ore with zinc content mined throughout the world last year.

Story is from mining.com

I’ll give you this, GDX looks better than GDXJ and silver miners, which doesn’t bode well for new highs without further consolidation or a lower low being made. In other words, I can’t see GDXJ and silver miners just all of a sudden taking off here and outperforming GDX. More likely GDX is going to be capped soon and the whole sector sells off.

Commodities (GCC) down today too.

Miners won’t take off until GCC bottoms, and right now the weekly GCC chart looks precarious. Next week, which will start a new monthly candle, is going to be very important.

pot shares jumped up today on news canada is targeting july 1 2018 for legalization.

6-20%.

New blasphemy law passes in Canada……..for lslam ….zerohedge

Time for the dominant religion to change Jerry.

Not gonna take as long as some people think. (if they even ponder yet)

Not that it matters but I figured it would happen about 2500. (the year)

But after hearing people saying they intend to have 6-8 kids ….per wife, and christians have maybe 2? (kids not wives.)

I just dont see it taking another 400 years.

I find it really interesting the facists of the 30-40s were the people defending christianity, and now they are supposedly so evil we cant even mention it.

Today, its Putin and Assad defending christianity, and look how evil we make them out to be.(not that they defend christianity more than other religions)

Really makes me wonder if religion isnt a bigger part than I have been giving it credit.

Commodities lower now than 1999, which was supposedly the end of a 20 year bear market.

Raw materials are cheaper now than they were 35+ years ago. Let that sink in.

Buying at a 35 year low sounds pretty good to me.

Matthew – That’s exactly what I was thinking when I read that. If the lows in Commodities are that historic, then it is time to load up.

April-july 1982 gold was about 300.

Had a person bought at that moment, arguably a great time to buy, held until today they made at todays price 1250? about?, 3-4 times their money, in 35 years.

Traders love it of course, preserve purchasing power? sure, ok, if you say so.

But compared to other investments? better and worse than some.

But people I know from 35 years ago said to heck with gold, real estate, and they are multi millionaires now AND own paid for multiple cash generating properties.

Lower mainland BC, some people consider the area desirable.

PMs could catch up, but 35 yrs is a bit of a wait.

I just think PMs should be kept in perspective.

Just saying, as a 35 year low was mentioned.

There was no reason to hold much gold between 1980 and 2000 so waiting shouldn’t have been anyone’s plan.

Everything swings from cheap to expensive and back again. Cycles never end.

Gotta disagree Mathew, but Im a sorta bug, 5% -10% phyzz, phyzz gold has it uses.(as u know)

My point is simply there have been better returns.

I know no one on here really likes to talk other than PMs, but check pizza joints the last few years. American market dominoes for example.

I dont own it, just sayin.

Agreed Matthew. Everything in its season and cycle.

of course there is, i forgot, check dollarrama too.

those 2 out of interest i mention as the time to buy was gold at about 1800.

gold down down down and dollarrama and dominos have made 1000%+

not including splits.

Ditto on the “everything in its season and cycle”

I think the final cycle for the pm is screwed up…….

no way anyone could have predicted ..QE and zero rates…….

aaand, no need to be concerned about envirnmental,geopolitical,cave ins, corrupt or plain lousy management, psychology etc etc.

just sit back and watch it grow.

The clues were there for anyone thinking.

Dollarrama is not dollarrama, its 20 rama, dominoes is a better choice for ALOT of people over restarants. For those watching shadowstats for example alot of people out of work.

So the clues were there.

I got dollar rama, Im not on the american market.

i think i mentioned dollar rama here,(10 years ago? when shares were first available.)

Thanks, Guys.

And the award for the dumbest politician in Idaho goes to:

State Rep Erpelding: Thank you, Mr. Speaker. I don’t have an opinion on this bill. However, I do have an opinion on facts. Facts are somewhat important… If we say that gold is going to protect us from inflation, I want to point out that in 1868, gold was $27 an ounce, and today gold is $1,218 an ounce. So, we can’t say that gold is going to protect us from inflation when you have that type of a price range over the last hundred years. So, I just want to point out that facts are important.”.