Weekly Key Reports Schedule

While this week is typically a slow trading week with Labor Day right around the corner there are some reports that will be of interest to traders and the Fed. Mostly dealing with job numbers here is a breakdown of the reports released this week.

…

The key report this week is the August employment report on Friday.

Other key indicators include the August ISM manufacturing index and August vehicle sales, both on Tuesday, and the July Trade Deficit on Thursday.

9:45 AM: Chicago Purchasing Managers Index for August. The consensus is for a reading of 54.9, up from 54.7 in July.

10:30 AM: Dallas Fed Manufacturing Survey for August.

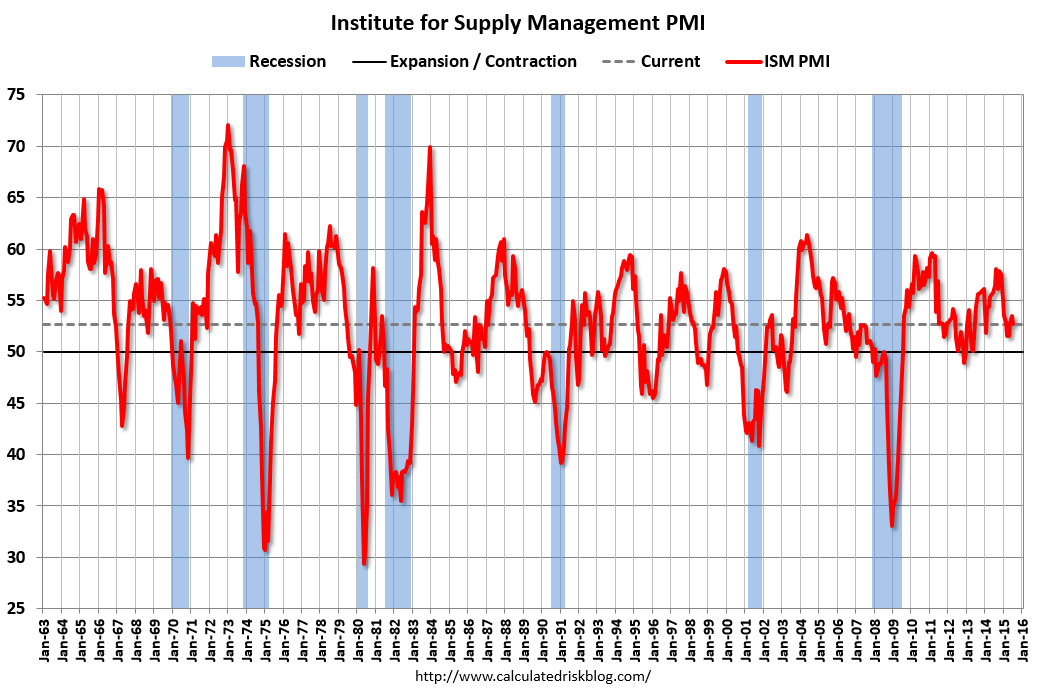

10:00 AM: ISM Manufacturing Index for August. The consensus is for the ISM to be at 52.8, up from 52.7 in July.

10:00 AM: ISM Manufacturing Index for August. The consensus is for the ISM to be at 52.8, up from 52.7 in July.

Here is a long term graph of the ISM manufacturing index.

The ISM manufacturing index indicated expansion at 52.7% in July. The employment index was at 52.7%, and the new orders index was at 56.5%.

10:00 AM: Construction Spending for July. The consensus is for a 0.8% increase in construction spending.

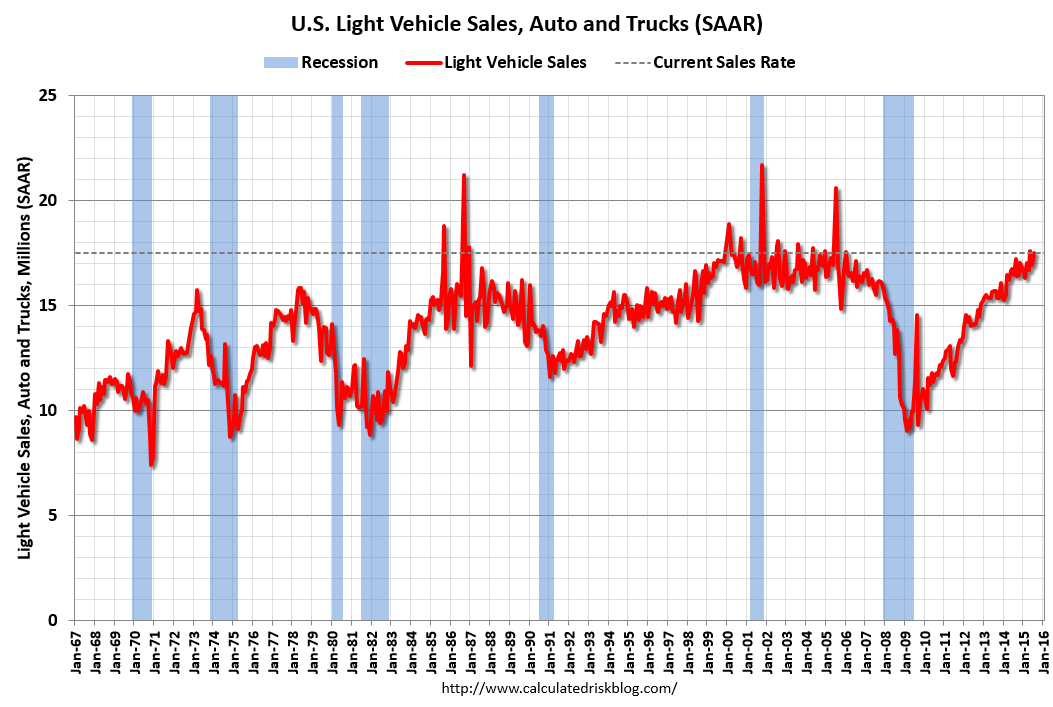

All day: Light vehicle sales for August. The consensus is for light vehicle sales to decrease to 173 million SAAR in August from 17.5 million in July (Seasonally Adjusted Annual Rate).

All day: Light vehicle sales for August. The consensus is for light vehicle sales to decrease to 173 million SAAR in August from 17.5 million in July (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the July sales rate.

7:00 AM: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for August. This report is for private payrolls only (no government). The consensus is for 210,000 payroll jobs added in August, up from 185,000 in July.

10:00 AM: Manufacturers’ Shipments, Inventories and Orders (Factory Orders) for July. The consensus is a 0.9% increase in orders.

2:00 PM: the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 273 thousand initial claims, up from 271 thousand the previous week.

8:30 AM: Trade Balance report for July from the Census Bureau.

8:30 AM: Trade Balance report for July from the Census Bureau.

This graph shows the U.S. trade deficit, with and without petroleum, through June. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is for the U.S. trade deficit to be at $42.9 billion in July from $42.8 billion in June.

10:00 AM: the ISM non-Manufacturing Index for August. The consensus is for index to decrease to 58.5 from 60.3 in July.

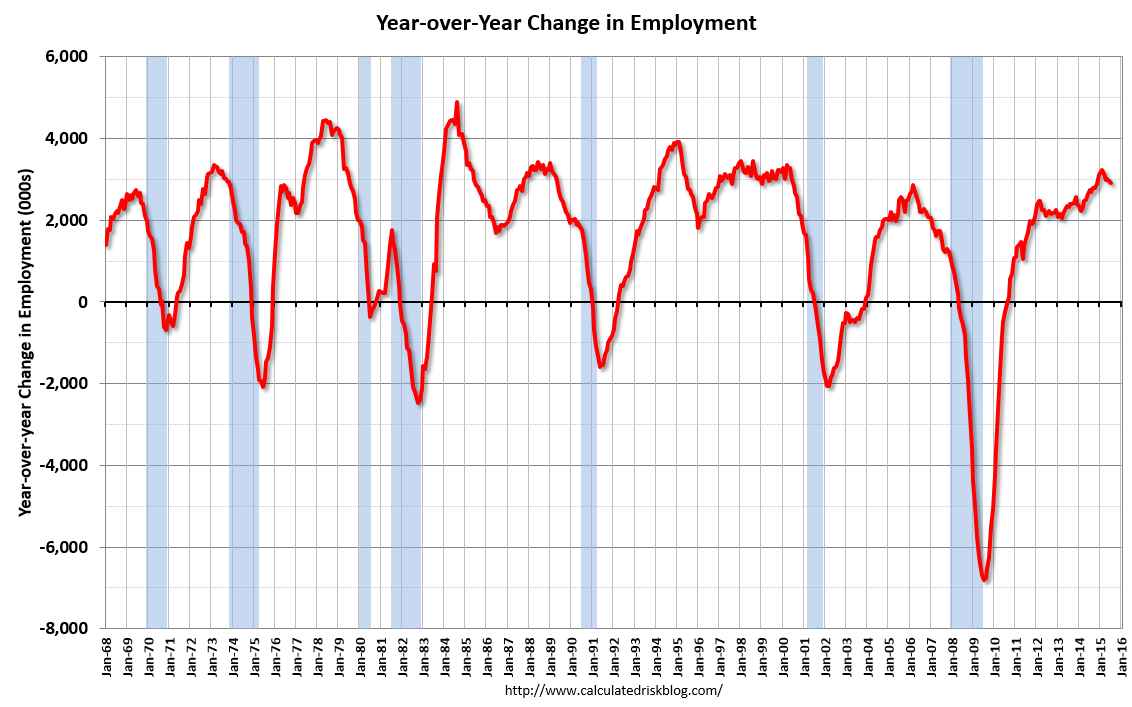

8:30 AM: Employment Report for August. The consensus is for an increase of 223,000 non-farm payroll jobs added in August, up from the 215,000 non-farm payroll jobs added in July.

The consensus is for the unemployment rate to decrease to 5.2%.

This graph shows the year-over-year change in total non-farm employment since 1968.

This graph shows the year-over-year change in total non-farm employment since 1968.

In July, the year-over-year change was over 2.9 million jobs.

As always, a key will be the change in real wages – and as the unemployment rate falls, wage growth should pickup.

That’s the spin the feds will need, higher wage growth! placing a Sept rate hike into play

Higher wages with lay offs, and time off , or reduction in hours……..Walmart , middle managers being effected….zerehedge

zere here zero……..

September shaping up as Fed’s worst nightmare

Jeff Cox – August 31, 2015

___________________________________________________________

Here’s an excerpt from the editorial:

“Bad Augusts frequently lead to bad Septembers, and in this case a particularly difficult backdrop for the Fed.

“Is the worst behind us? Possibly not. On Tuesday, we start a month with a bad reputation,” Sam Stovall, U.S. equity strategist at S&P Capital IQ, said in a note to clients Monday. “September is the only month in which the S&P 500 fell more frequently than it rose.”

Read MoreSeven reasons why the market has gone totally nuts

That’s bad enough in itself, but here’s another statistic from Stovall: In Augusts when the index fell more than 5 percent (it was down 6 percent by around lunchtime Monday) September followed with a decline 80 percent of the time, with the average drop almost 4 percent.

The rest of the macro picture doesn’t get any better.

While corporate profits overall in the second quarter ended up just above flat, the third quarter is expected to show a decline of about 4 percent, according to the latest numbers from S&P Capital IQ that are heading still lower. At the beginning of the year, quarterly earnings were projected to rise more than 6 percent for the period, so even if companies beat expectations by the usual 3 or 4 percentage points, that still makes for a dismal quarter.

The broader economic outlook isn’t much better, either. After a second quarter where gross domestic product unexpectedly jumped 3.7 percent, the third quarter is tracking at just a 1.2 percent gain, according to the latest reading from the Atlanta Fed. A stronger dollar, the slowdown in China and notoriously volatile payroll growth figures from August further compound things.

In short, the Fed appears to have missed its window for raising rates.”

http://www.cnbc.com/2015/08/31/september-shaping-up-as-feds-worst-nightmare.html

Personally, I still think the Fed may try a token 25-40 basis point rise by the end of the year, but surely they don’t want to be guilty of causing the next great depression by raising rates when the market can not absorb it. The embedded video in the article above made an interesting point about watching bank stocks for the indication of when the Fed may try to raise rates. Personally, I think a falling dollar scenario, as we’ve discussed quite often this year on the blog, will embolden them, but I just don’t see how they can try to raise rates in Sept with the perfect storm of problems mounting (China, Europe, US market extreme volatility, changing oil dynamics, and a general uncertain temperament by most investors).

oh yeah……and terrible Q3 number due to be reported, the fact the September is seasonally weak for the general markets, Shemitah worries (whether nonsense or accurate are on peoples minds)……and let’s not forget the millions of “experts” that have suddenly come out of the woodwork the last 2-3 months calling for a Sept. crash.

None of this sounds like a good time to raise interest rates. The challenges of an artificially propped market, that is hooked like an addict to zero interest rates are coming home to roost. Allowing investment institutions and banks to borrow at virtually nothing and juice the stock markets has been supported by almost everyone, because there are not any returns on deposit products like savings accounts, CDs, Money Markets etc…. The only place to go for returns has been the stock markets, so with everything teetering on the brink, then it’s not the best time to hike rates. The wonkiness has arrived!

This is not a report but one has to keep one’s head up for Sept 3 & 4th. These are Victory Days in China and the SSE market will be closed. If a paper contract crash on gold is going to happen it could happen later this week. Tying this in with the news on jobs etc gold/silver could end up with interesting numbers.