Andrew Pollard, President and CEO of Blackrock Silver (TSX.V:BRC – OTCQX:BKRRF), joins me to review the next batch of high-grade silver and gold intercepts returned from this year’s expanded 22,000 meter Measured and Indicated (M&I) conversion drill program on the 100% controlled Tonopah West Project, in Nevada. We also discuss the potential for expansion drilling, the rising grade profile, and timeline to permitting.

Highlights from this next batch of drill results:

- TXC24-095 returned multiple zones of high-grade mineralization including:

- 1.68 meters of 1,056 grams per tonne (g/t) silver equivalent (AgEq) [572.7 g/t silver (Ag) and 5.38 g/t gold (Au)] from 192.9 meters

- 1.83 meters of 341 g/t AgEq (147 g/t Ag and 2.61 Au) from 196 meters

- 1.07 meters of 633 g/t AgEq (343.7 g/t Ag and 3.21 Au) from 239 meters, including 0.55 meters of 1,225 g/t AgEq (665 g/t Ag and 6.23 g/t Au)

- and 5.03 meters of 774.5 g/t AgEq (461.5 g/t Ag and 3.47 g/t Au) from 242.5 metres, including 0.76 meters of 2,245 g/t AgEq (1,362 g/t Ag and 9.8 g/t Au)

- TXC24-098 returned 1.22 meters of 634 g/t AgEq (265.6 g/t Ag and 4.09 g/t Au) from 326.8 meters, including 0.3 meters of 2,480 g/t AgEq (1,034 gt Ag and 16.06 g/t Au)

- TXC24-117 returned 2.01 meters of 1,783 g/t AgEq (1,141 g/t Ag and 7.13 g/t Au) from 261.2 meters, including 0.4 meters of 6,064.4 g/t AgEq (3,712 g/t Ag and 26.13 g/t Au)

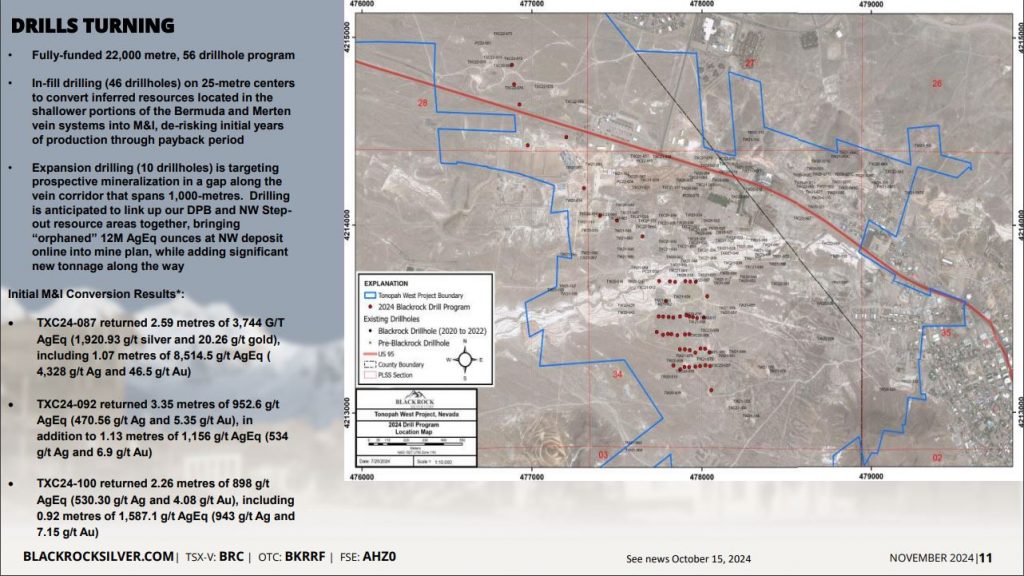

Andrew discusses how the goals of this drill program are to improve confidence in the continuity of mineralization in the deposit, converting Inferred mineralized areas Measured and Indicated, while connecting orphaned areas of mineralization, including the potential of bringing in the 12 million ounces of stranded ounces at the Northwest Step Out. Additionally, there is the goal to increase the resources and anticipated mine life a few years beyond the 8-year and 8.6 million annual production that was first outlined in the Preliminary Economic Assessment (PEA).

In that initial PEA at the base case gold price of $1,900 per ounce and silver price of $23 per ounce, the Project commands an after-tax net present value (“NPV”) discounted at 5% of $326-million on a low initial capex of $178-million (including $22-million contingency) with a payback of 2.3 years and an after-tax internal rate of return (“IRR”) of 39.2%, and an All-in Sustaining Costs (“AISC”) of $11.96 per silver equivalent ounce basis.

One of the other takeaways from the last two batches of drill results released is that the grade profile is actually increasing, with many results coming in higher than the average resource grade previously released to the market, and thus should be improving the economics as well. Andrew outlines that the plan is to keep drilling through 2024 into the first half 2025, and then updating the resources and PEA accordingly.

We wrap up having Andrew walk us through the advantages of being on private land in Nevada, the anticipated permitting timeline, and some of the improving sentiment for US-based projects under the Trump administration, which may offer more blue-sky upside on the surround BLM prospects in their land package. He feels their resources, preliminary economics, permitting path and ability to grow puts the Tonopah West Project in a unique position to separate from most other silver projects in the space, and potentially be attractive as an acquisition target to larger producers.

If you have any follow up questions for Andrew regarding Blackrock Silver, then please email us at Fleck@kereport.com or Shad@kereport.com.

- For full disclosure, Shad is shareholder of Blackrock Silver at the time of this recording.

.

Click here to visit the Blackrock Silver website to read over the recent news we discussed.

.

.