This article from Bloomberg helps to out the Trump rally in perspective. I personally think this rally that dates back to 2009 is all thanks to QE around the world. Yes there is optimism for tax cuts and the such but those do not have the same impact as free money… Now that the easy money spigot is being turned off (slowly) there will be a breaking point where buyers have no more access to pretty much free money. We are already seeing corporations scale back their share buybacks and insiders are selling. It won’t happen tomorrow but I am looking to mid next year as a time to determine if liquidity is drying up.

Click here to visit the original posting page over at Bloomberg.

…

Market gains since Election Day have been nothing out of the ordinary.

The other days, President Donald Trump shared a few thoughts about the stock market.

It would be really nice if the Fake News Media would report the virtually unprecedented Stock Market growth since the election.Need tax cuts

— Donald J. Trump (@realDonaldTrump) October 11, 2017

Like so many of the president’s statements, this one is objectively false. Our charge today is to set aside the political debate, and instead use his statement as an opportunity to explore ways to compare markets and rallies. Cognitive issues and innumeracy affect all investors, including presidents; this isn’t our first discussion of issues like denominator blindness, nor will it be our last.

Instead, we can use data to see how the so-called Trump rally compares to others.

No. 1. U.S. Presidential Rallies: As Bloomberg News reported the other day, “the ‘unprecedented’ stock market rally since his election right now isn’t big enough to crack the top five in presidential history.” As the accompanying chart shows, the Standard & Poor’s 500 Index has gained 19 percent 2016 election. That rates better than three other post presidential elections: George W. Bush in 2004 (7 percent), Bill Clinton in 1992 (10 percent), and Barack Obama in 2012 (16 percent).

Tallying Trump Rally

It’s ranked seventh-best in presidential history behind Kennedy.

However, the post Trump-election market has lagged others, in some cases by a lot. At 11 months after the election, the market under John F. Kennedy’s 1960 victory was up was 24 percent. That trailed Franklin D. Roosevelt’s 1944 rally of 28 percent. The next four presidents on the list all enjoyed rallies by this time in office that were about double or better than that of Trump’s: George H.W. Bush in 1988 at 31percent, Herbert Hoover in 1928 at 35percent, Bill Clinton (again) in 1996 at 38 percent, and Roosevelt (first election) in 1932 at a whopping 41 percent.

In other words, the Trump rally clocks in at No. 7. While that is pretty good — remember that markets fell after some presidents won election — it is hardly unprecedented.

Just as an aside — I am on record as reminding people that all presidents get too much credit when things go right and too much blame when they go wrong. Using market performance as a basis of presidential prestige or lack thereof is the refuge of partisan hacks and scoundrels.[ii]

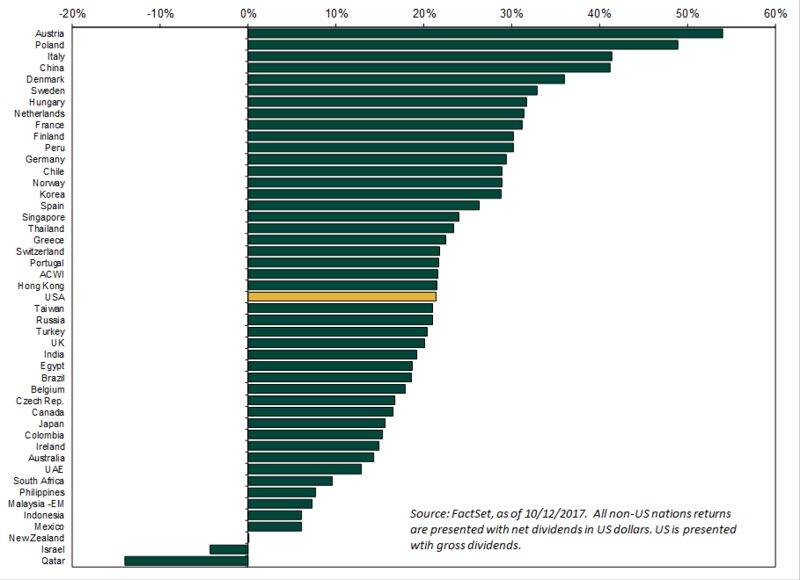

No. 2. Global Rallies: As we have discussed before, looking at a market rally in the U.S. while ignoring gains overseas is a foolish approach to performance analysis. Ken Fisher, of Fisher Investments, directs us to this table showing various country gains.

The U.S. rally is not only below the median, it lags other major countries such as Germany France, Italy, Spain — even Greece! The Trump Bump lags the Merkel bump, the Macron bump, even the Tsipras bump. Of course, U.S. markets had much bigger gains during the past decade than those countries. But rather than look for some political explanation, simple mean reversion accounts for much of the differences.

No. 3. March 2009: Speaking of which: The current rally in equities, inherited by the president, began when the market bottomed in March 2009, under Obama.

Radical Obama Was Going to Crash Markets

(Click the link above to see the chart) As you might have guessed, it is a market that went almost straight up.

That was pointed out on Twitter:

Quick look at the Trump rally in the $SPX which, interestingly, dates to March 2009. Weird. pic.twitter.com/cmifGpWfTv

— Invictus (@TBPInvictus) October 10, 2017

Another wag pointed out, tongue firmly in cheek, that must have been when Trump began contemplating running for president, and the market then efficiently incorporated this fact it into prices.

The president seems to be naïvely making absolute performance claims while ignoring the data on relative performance. Imagine a mutual fund or hedge fund manager making similar claims. The disciplinary fines would be enormous.

Either way, the investing public deserves better.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.